The annual reporting season commenced in Malta last week with the publication of the financial statements of HSBC Bank Malta plc. Given the record interim financial performance for the first six months of the year announced last August as well as the publication of the details of the Q3 performance later in the year, it was not surprising to see the headline figures of HSBC Malta last week.

The HSBC Malta Group reported a profit before tax of €154.5 million, which is 15.4 per cent higher than the pre-tax profit of €133.9 million generated in the previous year. Net profit reached a record of €100.1 million (equivalent to €0.2778 per share) which translates into a return on equity (ROE) of 17.5 per cent.

This is the second consecutive year with a double-digit ROE following a prolonged period of subdued returns as a result of the unfavourable interest rate environment. In fact, HSBC Bank Malta had not reported a double-digit ROE since 2013. Moreover, the return on equity of 17 per cent achieved in both 2023 and 2024 represents the highest returns for shareholders since 2008. In that period, the bank had reported three consecutive years of returns on equity above 20 per cent.

As indicated in some of my articles over the past two years, the two large retail banks in Malta benefited substantially from the surge in interest rates between 2022 and 2024. In fact, the main driver of the record financial performances of both HSBC and also BOV in 2023 and 2024 was the elevated interest rate environment across the euro area. Many other banks across the euro area also experienced a jump in their profitability levels leading to a remarkable surge in their share prices to multi-year highs.

HSBC Malta’s net interest income climbed by 5.2 per cent during 2024 to €206.1 million as a result of both the favourable interest rate environment as well as the higher level of average customer deposits held throughout the year. Nonetheless, it is good to note that the bank generated higher income also from other business areas, namely fee and commission income, foreign exchange as well as insurance operations.

Finally, it is pertinent to highlight that the 2024 financial performance of HSBC Malta was also boosted by the release of expected credit losses amounting to €14.6 million, which was higher than the release of €4.6 million in the previous year.

While the record financial performance was to be expected, the extent of the final dividend declaration may have been the main area of interest for the minority shareholders of HSBC especially in view of the recent developments which may be causing an elevated level of uncertainty regarding the course of action that the parent company will be taking as part of their ‘strategic review’ of Malta.

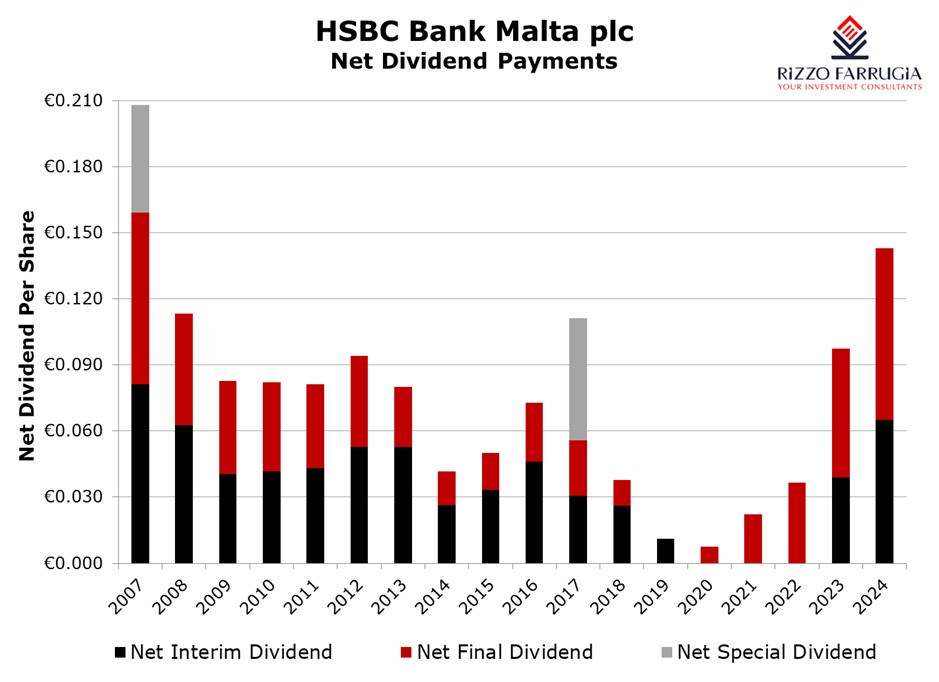

Following the net interim dividend of €0.065 per share paid in September 2024 (this was the highest interim dividend since 2007), HSBC Malta announced last week that its Board of Directors is recommending the payment of a final net dividend of €0.078 per share. This dividend will be among the items to be discussed during the upcoming Annual General Meeting being held on 13th May 2025 and if approved, the dividend will then be distributed to all shareholders on 20th May 2025.

As such, the total net dividend attributable for the 2024 financial year amounts to €0.143 per share, which represents a dividend payout ratio of 51.5 per cent (the highest dividend payout ratio since 2017). The total net dividend of €0.143 per share in respect of the 2024 financial year is equivalent to a net dividend yield of 9.1 per cent based on the current share price of €1.57. Investors across the Maltese equity market have not seen such an elevated dividend yield from companies listed on the Malta Stock Exchange for a considerable number of years.

The total net dividend of €0.143 per share is also the highest dividend distributed to HSBC Malta shareholders since 2007. At the time however, the dividend payout ratio was at a higher level of 75 per cent. Additionally, apart from the ordinary dividend distributions, HSBC had also embarked on a series of special dividends in those years which was a remarkably rewarding time for investors exposed to HSBC Malta shares.

Apart from the financial performance and the dividend distributions, the minority shareholders of HSBC Malta as well as other market participants would also have been understandably keen to receive further news on the strategic review by the HSBC Group on its Malta subsidiary. In the commentary to the Group-wide announcement last week also related to the publication of the 2024 annual financial statements, HSBC gave an update of the progress of the reshaping of the Group. They made reference to the disposals undertaken in various jurisdictions and other planned sales in Germany and South Africa. With respect to the Malta subsidiary, it was stated that the “review is at an early stage and no decisions have been made”.

This was also replicated by HSBC Malta’s CEO Geoffrey Fitche during a meeting with financial analysts last week wherein he confirmed that the management team in Malta is working on a ‘business as usual’ approach despite the strategic review. Moreover, the CEO commented that the bank is not feeling any impact at all so far on its current business operations.

As the financial performance of HSBC and many other euro area banks was boosted by the favourable interest rate environment in 2023 and 2024, there will inevitably be an impact with interest rates having declined from their peak of 4 per cent in June 2024. In fact, the European Central Bank (ECB) has already reduced interest rates five times since it started to cut rates in June 2024 taking its deposit rate to 2.75 per cent. A further interest cut of 25 basis points is widely anticipated during the upcoming monetary policy meeting of the ECB next week (6 March).

HSBC Malta has reported some good progress on its balance sheet repositioning in order to reduce the impact from changes in interest rates. The financial statements as at 31st December 2024 show a sizeable shift in cash balances (-36 per cent to €1.07 billion) to a portfolio of financial investments which increased by 74 per cent (or €975 million) to €2.29 billion. This would protect the interest income to be received as interest rates have started to decline. Nonetheless, one of the only disappointing highlights of the financial performance was a 6.8 per cent decline in customer loans (equivalent to €211 million) to €2.87 billion.

Despite the inevitable decline in profitability that ought to be seen in the financial performance of HSBC Malta during the course of 2025 from the elevated levels over the past two years, the focus will undoubtedly remain on both the dividend distribution levels as well as news on the strategic review taking place.

Minority shareholders should be comforted by the elevated capital ratios of HSBC with a Tier 1 capital ratio increasing to 22.6 per cent. In fact, HSBC Malta’s CEO also remarked last week that the bank is “clearly overcapitalised”. This should lead to continued strong dividends to shareholders until such time that the strategic review is indeed concluded.

Read more of Mr Rizzo’s insights at Rizzo Farrugia (Stockbrokers).

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Will the ‘magnificent seven’ become the ‘peace makers’ between the USA and Iran?

Financial markets have always had a seat at the table in wartime

Maltese MEPs hail EU anti-corruption law as milestone for business transparency

EU countries will now be required to align their national legal frameworks

Investing in times of war

What does Warren Buffett teach us about investing during conflicts?