Following the successful Malta Government Stock (MGS) offering earlier this month, the total issuance so far this year has surpassed €1 billion, thereby bringing the total MGS issuance (the main part of Government debt) to €9.16 billion. The issuance of over €1 billion in MGS’s is in line with the Government requirements as announced in the Budget last year.

An analysis of the statistical results published by the Treasury last week following the closure of the MGS offer period provides some important findings, especially when viewed in the context of the other MGS offerings over the past 18 months.

The applications from those classified as retail investors (up to €500,000 per application) during this month’s MGS offering amounted to around €90 million with a clear preference for the longer-dated security. In fact, applications for the six-year bond (the 2.8 per cent MGS 2030) amounted to a mere €11.4 million while the 10-year bond (the 3.25 per cent MGS 2034) attracted over €78 million.

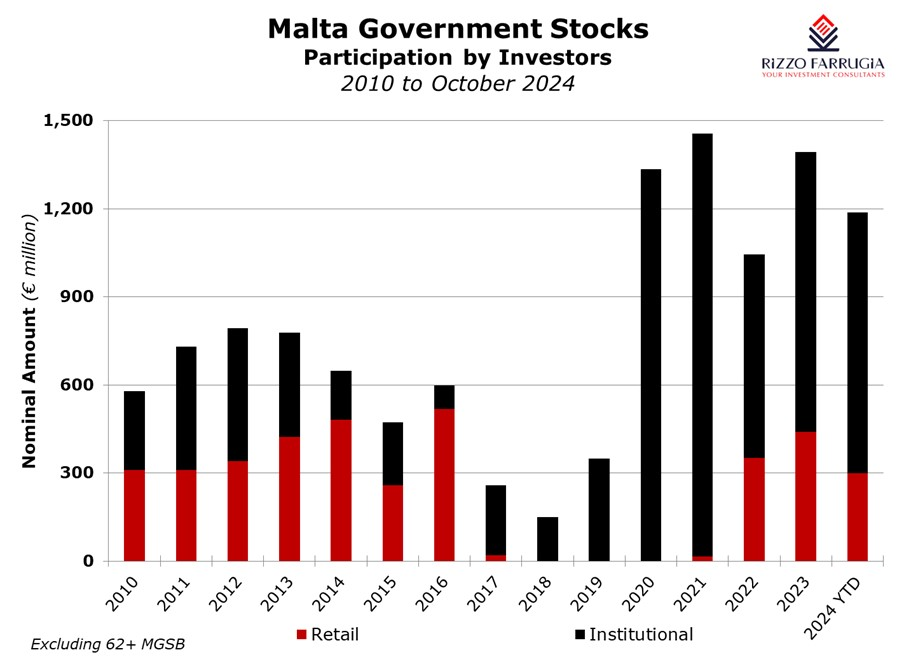

At €90 million, participation by retail investors was the lowest so far across the three MGS offerings this year (the February 2024 issue attracted retail applications totalling €108 million and the July offer attracted €102 million). When extending the comparison to the MGS issuance during 2023, the €90 million exceeds the amount raised in September 2023 of €81.6 million (which was ill-timed coming only a few weeks after the July 2023 issue) but was far lower than the retail issuance in February 2023 and July 2023 with participation of over €180 million in each case.

Apart from the lower take-up by retail investors over recent months, the other evident trend is that retail participation has clearly shifted towards longer dated maturities, reflecting expectations of lower interest rates.

While in the first two MGS issues in 2023, there was very strong take-up in the short-term securities (three and five-year bonds), the longer-term bonds issued in 2024 attracted most of the participation by retail investors. It is interesting to highlight that the offering that attracted the highest retail participation since the start of 2023 was the 3.55 per cent MGS 2026 (a three-year bond), which attracted a sizeable amount of €111.6 million also exceeding the latest October 2024 offering across both securities of €90 million.

Retail investors are therefore preferring to lock in fixed rates for a longer period of time as interest rates across the eurozone are expected to decline further in the months ahead despite the three rate cuts by the European Central Bank (ECB) so far this year of 0.25 percentage points in each of June, September and also October. Following such decisions, the ECB reduced its deposit facility from four per cent to 3.25 per cent.

In view of expected further declines in the ECB interest rate in the weeks and months ahead, there is a high probability that the yield on a 10-year MGS issue in the coming months would be below prevailing rates. In fact, in September 2023, the coupon of the 10-year MGS was at four per cent which was reduced to 3.5 per cent in August 2024 and dropped again to 3.25 per cent in October 2024.

While participation by retail investors has been on the decline (the coincidental approval of the new five per cent bonds by Bank of Valletta plc on the same day of the opening of the MGS offer period could also have impacted this), the most recent MGS offers in August and October attracted record amounts from institutional investors, clearly signalling that financial institutions holding substantial amounts of liquidity are participating in Malta’s sovereign bond market.

In fact, when reviewing the total MGS issuance of €1.2 billion so far during 2024, as expected, this was mainly allotted to institutional investors (€886.7 million) with the balance of €300.3 million taken-up by retail investors.

In particular, those institutions classified as ‘Resident Credit Institutions’ (essentially local banks) are the largest participants in the market. In the latest MGS issue earlier this month, 68 per cent of the total issue of circa €400 million (or 88 per cent of the auction) which is equivalent to €271 million nominal, was allotted to resident credit institutions. There was higher demand for the 10-year than for the six-year, highlighting that these same credit institutions also want to lock-in to current yields on longer-term bonds. This provides them with an opportunity to enjoy recurring interest income for the medium to long term at essentially very low levels of risk given Malta’s strong credit rating and robust financial dynamics with a debt-to-GDP ratio of 46.7 per cent as at the end of June 2024.

The high participation of credit institutions in the MGS offerings over recent years was very evident in the balance sheet optimisation process being conducted by Bank of Valletta plc. As Malta’s largest bank, it undoubtedly holds the largest amount of local sovereign debt. The financial statements published by BOV semi-annually clearly show the effective management of their balance sheet through which a substantial amount of its balances with the Central Bank were shifted into bonds listed on both the Malta Stock Exchange (MGS’s) and also across international stock exchanges. In view of the changing interest rate landscape, BOV reduced its liquidity with the Central Bank from over €5.2 billion in 2021 to €1.2 billion as at 30th June 2024 with the resultant increase in the bank’s proprietary treasury portfolio to €6.1 billion. The importance of this will be evident in future reporting periods as the bank will be less susceptible to declines in interest rates.

Following the MGS issuance of just under €1.2 billion so far this year, it will be interesting to delve into the updated figures of the Government finances that will be presented as part of the Budget Speech next Monday 28th October. The Budget forecasts being tabled next week should not only indicate the expected issuance of next year and subsequent years but also update the market with respect to plans for any additional requirements in the final months of 2024. This is important since at this time last year it was envisaged that the Government would need to raise €1.7 billion in 2024 so unless the Government deficit has reduced materially, another large MGS issuance is required in the next few weeks.

Read more of Mr Rizzo’s insights at Rizzo Farrugia (Stockbrokers).

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Related

APS Bank continues to gain market share

APS is Malta’s third largest bank in terms of total assets but second largest in loans

CrediaBank aims to ‘supercharge’ Malta

The upcoming plans by CrediaBank could prove to be important for the Maltese banking sector and the domestic capital markets

A Liquidity Provider for the corporate bond market

Edward Rizzo suggests the Malta Development Bank could play an important role in revitalising the secondary market for corporate bonds