Malta’s full-year earnings season continued last week with a number of announcements. Undoubtedly, the most important one was from Bank of Valletta plc given its dominance in the banking sector and also since it is the largest capitalised company on the Malta Stock Exchange with a market cap exceeding €1.3 billion.

BOV implemented a marked changed in its communications and investor relations strategy over the past few years with the publication of quarterly financial statements and detailed analyst briefings. While the headline figures in the annual financial statements published last week may not have been a surprise to those who closely follow the quarterly announcements, a number of important observations emerge from the 2025 Annual Report.

Profitability above guidance

The BOV Group’s pre-tax profit in 2025 reached €260.4 million exceeding the upper limit of profitability guidance which was originally established between €200 million and €250 million at the beginning of the year and subsequently upgraded to a range of €215 million to €250 million at the half-year stage.

While the 2025 profit represents a decline of 13.9 per cent from the record pre-tax profit of €302.4 million in 2024, the performance must be analysed in the context of the interest rate declines by the European Central Bank (ECB) from the peak of 4 per cent until June 2024, the accelerated investment programme in technology and human capital pushing operating costs higher, as well as the marginal net impairment charge of a mere €0.04 million in 2025, compared to the net reversal of €23.8 million recorded in the previous year which was a substantial boost to profitability last year.

Balance sheet repositioning

The key item that helped BOV report such a strong profitability in 2025 despite the three factors highlighted above, was that net interest income rose to €387.4 million. The net interest income is the difference between what the bank earns on its loans, investments and central bank balances and what it pays on deposits and other funding.

Although the net interest income of €387.4 million was only a marginal increase from the €386 million recorded in 2024, this is 10 per cent higher than the €352 million generated in 2023 despite the significant downturn in the deposit facility by the ECB since then. This is a direct result of the balance sheet repositioning strategy that BOV’s management team has been very successfully executing since 2022.

The core of the strategy was the migration of assets away from short-term, variable-rate instruments (principally overnight deposits with the Central Bank of Malta) and into longer duration, fixed-rate assets comprising sovereign and investment-grade bonds held in the bank’s proprietary treasury portfolio (which has grown to €6.9 billion at an effective interest rate of 2.3 per cent), and customer loans with fixed or partially fixed interest rate structures. The increaased duration of the treasury portfolio to lock in higher yields has clearly cushioned the impact of ECB rate cuts in 2025.

Growth in market share

The pace of balance sheet expansion was another key highlight in 2025. Total assets rose by €1.4 billion to above €16.5 billion clearly showing the scale of BOV’s systemic role within the Maltese banking system.

The expansion of the balance sheet was driven by two principal forces. Customer deposits increased by €937 million during 2025, bringing the total deposit base to above €13.7 billion. The deposit base had already climbed to €12.8 billion at end-2024 from €12.1 billion a year earlier. In parallel, long-term liabilities rose by €277 million, following the successful issuance of Tier 2 subordinated bonds during the year under the Euro Medium Term Note programme which improved the Group’s capital ratios and diversified its funding profile.

On the asset side, the 16 per cent increase in the loan book to €8 billion is an important achievement in 2025 with BOV’s Chairman stating that the strong growth in the loan book also reflects specific circumstances currently taking place across the banking sector.

The repositioning away from low-yielding central bank reserves and towards loans and investments has been the defining strategic decision of the past three years. The loan-to-deposit ratio increased to 58 per cent in 2025 from 44 per cent in 2022. Liquidity held with the Central Bank of Malta declined to €920 million in 2025 from €4.6 billion in 2021 with the treasury portfolio rising to €6.9 billion from €3.5 billion in 2022.

BOV’s dominance in the banking sector is evident from the 49 per cent share of customer deposits, a share of 42.8 per cent of home loans, 51 per cent of corporate loans and 55 per cent in personal loans.

Stability in dividend

The overall dividend for the 2025 financial year is unchanged from the distribution in respect of the 2024 financial year (adjusted for the bonus shares) as the payout ratio increased from 42.6 per cent to 49.4 per cent which is precisely in line with the current dividend payout policy set at a maximum of 50 per cent of profit after tax.

BOV’s Board of Directors is recommending a final net ordinary dividend of €0.0659 per share and a special net dividend of €0.0105 per share (reflecting the portion of 2025 profitability that exceeded the profit before tax guidance of €250 million). Both dividends, amounting to €0.0764 per share or €49 million in total, will be paid on Friday 12 June 2026 to all shareholders as at close of trading on Thursday 7 May 2026.

Coupled with the net interim dividend of €0.0556 per share paid in September 2025, the total net dividend attributable for the 2025 financial year amounts to €0.132 per share.

The stability of the total net distribution of €85 million for the 2025 financial year must be seen in the context of the transformation in recent years from a bank that was unfortunately constrained in its distributions by legacy issues and regulatory uncertainty to one that is now proactively returning capital through multiple avenues. This represents one of the most significant governance improvements across the local equity market in recent years.

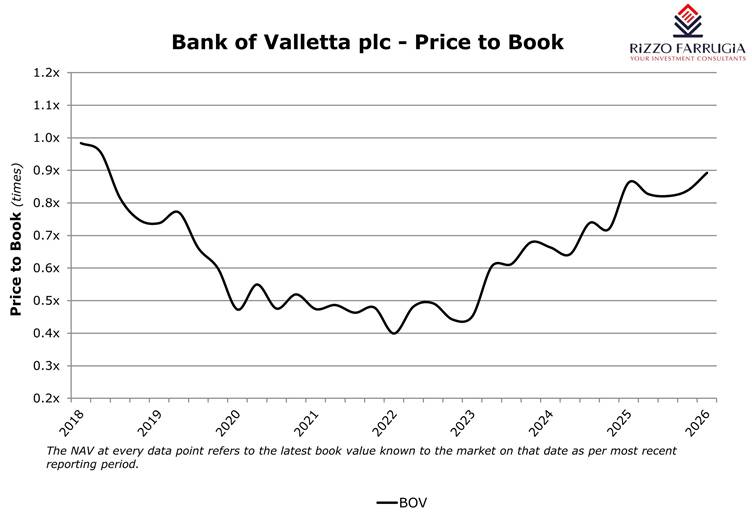

Re-rating of share price

There was an evident re-rating of the share price of BOV over the past three years with the shares jumping higher as the price to book multiple rose from 0.45 times in Q1 2023 (55 per cent discount to book value) to a current level of 0.90 times book value (10 per cent discount).

Despite the strong upward movement in the share price over the past three years, BOV shares still trade on a single-digit price to earnings multiple (6.9x) and a 10 per cent discount to its December 2025 book value of €2.33 per share.

BOV has a very well-capitalised balance sheet (CET1 ratio of above 20 per cent), a clear dividend distribution policy and has reported a marked improvement in the non-performing loan ratio to 1.7 per cent. Given its dominant market position in Malta and indications that it will manage to maintain a double-digit return on equity, there is further scope for the share price to reduce the valuation gap with other eurozone banks which mostly trade above their book value.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Will the ‘magnificent seven’ become the ‘peace makers’ between the USA and Iran?

Financial markets have always had a seat at the table in wartime

Maltese MEPs hail EU anti-corruption law as milestone for business transparency

EU countries will now be required to align their national legal frameworks

Investing in times of war

What does Warren Buffett teach us about investing during conflicts?