We have always witnessed the same story-pattern: War breaks out → markets panic. Bombs fall → stocks tumble.

It is a one-way street. Geopolitics drives finance. But watching the Iran conflict unfold over the past four weeks, something feels fundamentally different. What if this time, the street runs the other way?

I confused you, right?

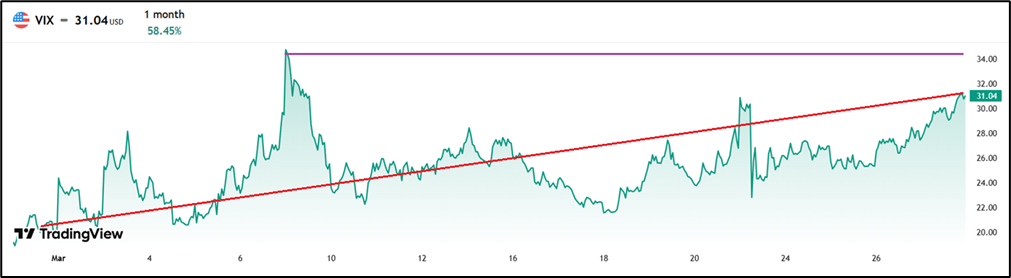

Since US and Israeli forces launched their first strikes on 28th February, Wall Street has been in freefall. The S&P 500 has notched five straight weeks of losses, its longest losing streak in nearly four years. The Nasdaq has slid into correction territory, down more than 10 per cent from its October peak, closing on 27th March at 20,948. The Dow has also entered correction, ending the week at 45,166.

The "Magnificent Seven" tech giants alone (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla) shed roughly $870 billion in market cap in a single week. Meanwhile, US crude oil is up more than 40 per cent since the war began, with Brent crude surging past $107 a barrel. The OECD has revised its US inflation forecast for 2026 sharply upward, from 2.8 per cent to 4.2 per cent, a figure that makes Federal Reserve rate cuts a distant dream and borrowing costs a growing nightmare for the American economy.

These are the facts. The damage is real, measurable, broad and accelerating.

But here is where it gets interesting.

Let’s look closely at the timeline of military decisions. A pattern emerges that is hard to dismiss.

Trump postponed planned strikes on Iranian power infrastructure on March 23. Just 15 minutes before the announcement, $580 million in bets on falling oil prices were placed in the futures market, later triggering insider trading allegations. 57 minutes later, Iran denied that there were ‘talks’ and the market collapsed. 57 minutes worth more than $3 trillion on the S&P500!

When talks showed signs of life, markets bounced. When they collapsed, markets crashed. Trump then extended his deadline for Iran by a further ten days, giving Tehran until 6th April to comply, a decision that came precisely as stocks were registering their worst weekly losses since the war began.

The sequencing is striking. Each military pause, each extended deadline, each carefully worded statement about "negotiations going well", they all arrive at moments of maximum market stress.

It no longer looks like just a coincidence, right?

The conventional framing, that war causes market volatility, is clearly true. But the more provocative thesis is that causality now runs in both directions and perhaps the more powerful direction is the reverse: Markets are actively shaping the war's tempo, its compromises and its eventual resolution.

As market strategist Jim Bianco observed, "only statements from the Iranian side move markets meaningfully now; Trump's proclamations have become white noise." Meaning the market has developed its own intelligence on this conflict, ignoring meaningless statements from politicians.

This is not entirely new. Financial markets have always had a seat at the table in wartime. But what is now different in 2026 is the speed, the visibility and the sheer scale of the feedback loop. Every general and diplomat can see in real time exactly what their words and actions cost or gain in market cap. When a single week of hesitation vanishes nearly a trillion dollars from America's biggest companies, that is not just background noise, that is a pressure campaign, and it runs 24/7 365 days a year with no ceasefire.

So, it turns out that the markets have become the most powerful key players in this war, not because they want peace, but because they cannot afford the alternative.

Equity participation on the MSE

Meaningful reforms are still needed to revive investor confidence

Malta’s dividend league table

Most retail investors nowadays have an overriding preference to invest in bonds

Continued operating progress at Farsons

Farsons’ beverage business delivered another year of record revenue and higher profitability in FY2025/26