The proposed digital euro could remove one of the most common frustrations in payments – waiting for refunds – by introducing “conditional payments” that only process once a service is delivered, according to European Central Bank officials.

In a joint article, Piero Cipollone and Frank Elderson outlined how the digital currency could enable payments that are automatically triggered when predefined conditions are met.

They illustrated this with a practical example: a train ticket would only be charged if the journey actually takes place. If the train is cancelled, the payment would never go through – eliminating the need for refunds altogether.

A shift in how payments work

The concept of conditional payments is being positioned as one of the digital euro’s most tangible innovations, allowing transactions to be embedded with logic that reflects real-world outcomes.

According to the ECB, this would be made possible through a unified European payments infrastructure, enabling such services to work seamlessly across the euro area.

The officials argue that this could significantly improve user experience while also opening the door for more advanced financial services built on top of the system.

Addressing concerns from the banking sector, the ECB stressed that commercial banks would remain central to the ecosystem rather than being sidelined.

Banks are expected to manage digital euro accounts and maintain direct relationships with customers, preserving access to key financial data used for lending and risk assessment.

At the same time, the digital euro is being framed as a platform on which banks can build new services – particularly value-added offerings that could generate additional revenue streams.

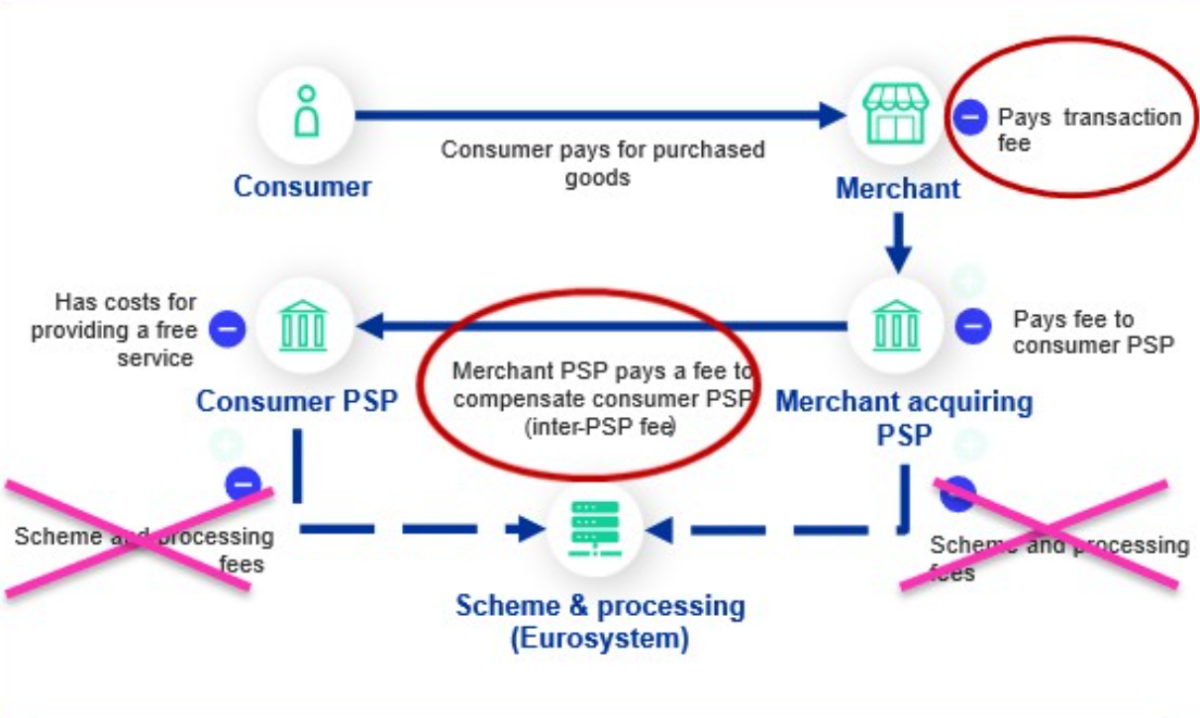

The ECB noted that banks would be remunerated under a dedicated compensation model built into the digital euro framework, ensuring they are paid for distributing the currency and providing related services. At the same time, overall costs are expected to decrease, as the system would eliminate scheme and processing fees typically charged by intermediaries.

Source: Piero Cipollone / Digital euro – AIB Executive Committee Meeting

Reducing dependence on non-European players

A key strategic argument behind the digital euro is reducing Europe’s reliance on international payment providers such as Visa and Mastercard.

Currently, many euro area countries depend heavily on these systems, particularly for cross-border and e-commerce transactions, often incurring higher fees and limiting Europe’s control over its payment infrastructure.

The ECB argues that a digital euro would strengthen “strategic autonomy” by providing a European alternative, while allowing banks to retain more of the fees currently paid to external providers.

Costs and rollout timeline

While some banks have raised concerns about implementation costs, the ECB estimates total investment at between €4 billion and €5.8 billion – significantly lower than some external projections.

These costs, the ECB said, could be offset over time through efficiencies, shared infrastructure, and reduced reliance on intermediaries.

Looking ahead, the Eurosystem expects to define common technical standards for the digital euro by this summer. However, full rollout remains contingent on the adoption of EU legislation, which is still pending.

Overall, the ECB positions the digital euro as both a defensive and forward-looking measure – aimed at safeguarding financial stability while ensuring Europe remains competitive in an increasingly digital payments landscape.

At its core, however, a system is promised where payments better reflect real-world outcomes – and where consumers no longer have to wait to get their money back.

Featured Image:

The European central Bank / CC BY-SA 3.0 DE

How Mediterrania Capital Partners is bridging private equity and public markets to unlock Africa’s potential

ASEF is reshaping how institutional investors think about Africa’s public markets: a growth engine and a diversifier in global portfolios

BNF Bank and Mastercard partner to bring added value to Maltese customers

Collaboration enhances everyday banking through exclusive experiences, rewards, and innovative payment solutions

ĠEMMA launches new podcast series to make financial literacy accessible for all

New episodes will be released every two weeks and will be available across multiple platforms