The full-year financial reporting season commenced in Malta last week with the publication of the financial statements of HSBC Bank Malta plc and Malta International Airport plc (MIA).

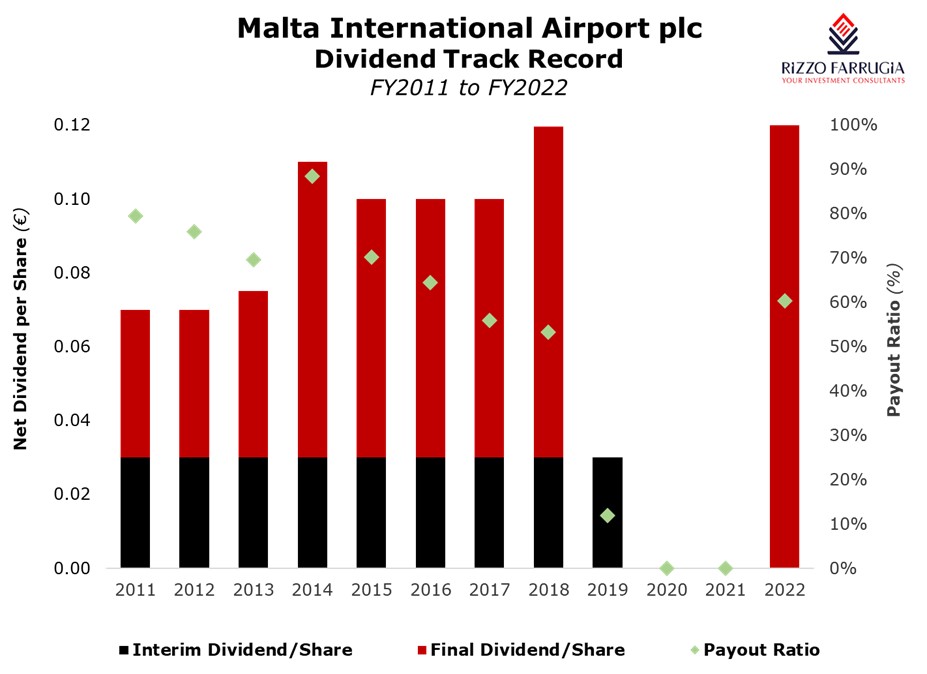

Since the airport operator publishes key financial highlights on a quarterly basis and also provides traffic and financial projections for the financial year, the key focus of last week’s announcement was the decision by the board of directors on whether dividends will resume after three calendar years (2020-2022) when no dividends were distributed to shareholders. The last dividend payment by MIA was in September 2019 amounting to €0.03 net per share and related to the interim dividend for the 2019 financial year.

Thankfully, following the very strong recovery in passenger volumes evident from April 2022 which translated into an equally strong recovery in the company’s profitability, the board of directors recommended a net dividend of €0.12 per share in respect of the 2022 financial year.

In order to put this dividend into a historical perspective when MIA regularly paid dividends to shareholders ever since the initial public offering (IPO) in 2002 until the start of the COVID-19 pandemic in early 2020, the company had last paid a full-year dividend of just below €0.12 per share (€0.1197 per share to be precise) in respect of the 2018 financial year. As such, the dividend being proposed for approval by the company’s shareholders during the upcoming annual general meeting (AGM) scheduled for 10th May 2023 matches the record distribution of some years ago. It is also worth pointing out that following the net interim dividend of €0.03 per share paid in September 2019, on 26th February 2020, the company’s board of directors had proposed a net final dividend of €0.10 per share for the 2019 financial year. This had subsequently been cancelled on 22nd April 2020 due to the pandemic.

The full-year net dividend of €0.12 per share proposed last week equates to a total payment of €16.2 million and translates into a dividend payout ratio of 60 per cent when excluding the significant tax credit which boosted the company’s financial performance in 2022. Incidentally, this dividend payout ratio is in line with the strategy of MIA’s parent company Flughafen Wien AG (Vienna Airport) who earlier this year confirmed that it will maintain its dividend payout ratio of “at least 60 per cent of the net profit”.

When reviewing the 2022 financial performance of MIA, it is interesting to note that the actual figures were very much in line with the guidance provided by the company in November 2022. At the time, MIA had substantially upgraded its traffic and financial figures published in July 2022 as a result of the better-than-expected recovery in passenger volumes during the peak summer period.

Actual revenues generated by the airport operator during 2022 of €88 million compare favourably with the November 2022 guidance of ‘over €85 million’. Similarly, the actual EBITDA amounted to €54.9 million (guidance of ‘over €52 million’) and the net profit before the €12 million tax credit of €26.8 million is also in-line with the indication of ‘over €25 million’.

Earlier this year, MIA had already published its traffic and financial targets for 2023. The airport operator expects passenger movements to grow by 7.7 per cent to 6.3 million which is equivalent to an 86 per cent recovery of the record pre-pandemic traffic in 2019. Based on the traffic projections being envisaged for 2023, the company aims to generate revenues of €97 million during the current financial year ending 31st December 2023, leading to an EBITDA of €59 million and a net profit of €29 million.

Should this financial performance be achieved and if the company maintains its dividend payout ratio at 60 per cent, it would translate into an overall dividend of circa €18 million for 2023 which is equivalent to a net dividend of circa €0.13 per share. Incidentally, the total dividend during the record year of 2019 had the final dividend not have been cancelled in early 2020, would also have amounted to a total of €0.13 per share. Although the company has a very large investment programme in the next few years, the dividends must be seen within the context of the current structure of the balance sheet. MIA has no interest-bearing borrowings (bonds or bank loans) and ended the 2022 financial year with liquidity of €68.7 million.

Since MIA publishes its traffic results on a monthly basis it is fairly easy for the numerous shareholders to monitor the ongoing performance of the company. It would also be interesting to see in due course whether the traffic and financial targets for this year would need to be revised during the summer period based on the airline capacity for the busy summer period and the actual results achieved in the months ahead. Prior to the onset of the pandemic in early 2020, MIA regularly upgraded their full-year guidance during the summer months.

Read more of Mr Rizzo’s insights at Rizzo Farrugia (Stockbrokers)

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

GO’s growing cash flow from Malta

During 2025, total revenue of the GO Group revenue rose by 3.9% to €254.4 million

Volatility across the Magnificent 7

All 7 equities had suffered double-digit percentage declines over recent months

Surge in sovereign bond yields

Why sovereign bonds defied their traditional ‘safe haven’ status in March