The offer period for retail and institutional investors in the two new Malta Government Stock issues (maturing in 2033 and 2038) came to an end last week and on Thursday afternoon, the Treasury published the preliminary results of the third MGS offering of 2023.

As I opined in my article last week, an analysis of the take-up by both retail as well as institutional investors is very important in the context of the overall borrowing requirements for this year totalling €1.6 billion as well as the timing of this latest offering so soon after the €400 million issuance in July 2023.

On Thursday, the Treasury announced that it will be allotting a total of €303.5 million (nominal) thereby falling short of the maximum issuance amount of €400 million (nominal).

Subscriptions from retail investors amounted to around €81.5 million (nominal). The Treasury explained that the final nominal amount that will be allotted to retail investors (which will be accepted in full) for each MGS will be published once the vetting of all applications is completed.

The demand of €81.5 million by retail investors is a weak result. In the previous two MGS issues this year that took place in February 2023 and July 2023, coincidentally retail investors subscribed to circa €180 million each time. Meanwhile, last year there was exceptionally strong demand from retail investors in October 2022 totalling €293.4 million when the Treasury had offered investors a 4 per cent yield for a 10-year bond. Prior to the October 2022 MGS issue, the Treasury had raised €57.7 million from retail investors in July 2022 but at the time, yields were at far lower levels than those prevalent nowadays.

In the press release issued last Thursday, the Treasury also confirmed that it will be allotting a total of €222 million (nominal) to institutional investors. The statistics published by the Treasury indicate that €217 million are being allotted to institutional investors in the 4.00 per cent MGS 2033 (IV) and only €5 million in the 4.30 per cent MGS 2038 (II).

Two interesting findings emerge from the analysis of the bids placed by institutional investors. In the 10-year bond, the 4.00 per cent MGS 2033 (IV), which attracted the large majority of participation, the weighted average price of the accepted bids of 98.999 per cent (which translates to a YTM of 4.12 per cent) was well below the fixed offer price to retail investors of 100.75 per cent (which translates to a YTM of 3.91 per cent). The accepted tenders by institutional investors in the auction process varied from a high of 101.40 per cent (translating into a yield-to-maturity of 3.83 per cent) to a cut-off price of 97.67 per cent (YTM: 4.28 per cent).

The other interesting observation in the 10-year MGS auction was that a large majority of the accepted bids totalling €150 million are being allotted to local credit institutions. This gives an indication of the strategy by a number of local banks to begin lengthening the duration of their Treasury portfolio in order to lock-in yields at current levels thereby protecting themselves from any eventual decline in the deposit facility by the European Central Bank.

The response by the institutional investors in the 15-year MGS was similar to that of the 10-year bond. In fact, the weighted average price of the accepted bids of 100.685 per cent (which translates to a YTM of 4.24 per cent) was also well below the fixed offer price to retail investors of 102.00 per cent (which translates to a YTM of 4.12 per cent) while the cut-off price was of 99.50 per cent (YTM: 4.34 per cent).

The institutional investors are clearly demanding higher yields which is a clear signal to the Treasury as well as to the other issuers seeking to tap the market in the weeks and months ahead.

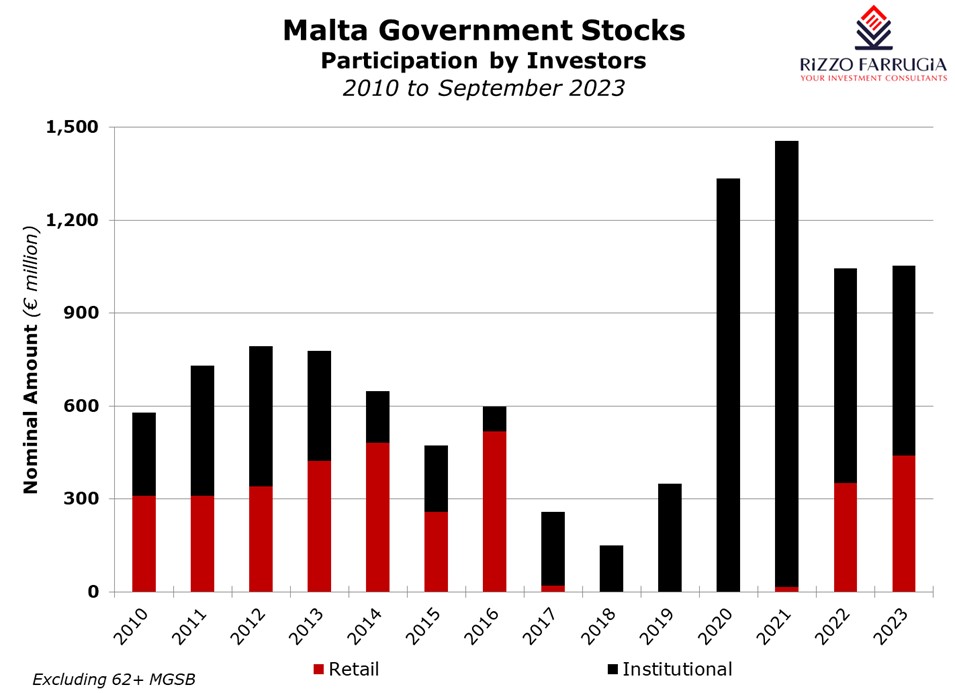

While the take-up of €81.5 million by retail investors last week is a low figure, this also must be analysed in the context of the total amount raised from retail investors this year. In fact, retail MGS issuance so far in 2023 at €440.7 million is elevated when compared to statistics for prior years. The record amount of MGS issuance to retail investors was in 2016 at €517.9 million followed by €481 million in 2014. In those years however, retail investors were enjoying immediate capital gains as a result of the decline in yields brought about by the quantitative easing programme of the European Central Bank.

Following this latest MGS issue, the total amount raised by the Treasury in MGS so far in 2023 amounts to €1,052.2 million (excluding the 62+ Malta Government Saving Bond) with institutional participation at €611.5 million and retail investors subscribing for €440.7 million. In view of the announcement at the start of the year by the Treasury that the total amount of MGS issuance during 2023 will not exceed €1.6 billion, Government officials at the Treasury should urgently clarify the overall remaining amount required to be raised this year. Retail and institutional investors both require clarity on the remaining funding requirement by the end of the year.

Regular communication by Government officials on overall funding needs is also important in the context of the elevated MGS issuance anticipated in the years ahead in view of the fiscal deficit as well as the refinancing of MGS redemptions. In fact, the Financial Estimates published last year indicate that following the record issuance projected at €1.6 billion in 2023, the Treasury will require an additional €1.3 billion in 2024 and €1.25 billion in 2025.

Read more of Mr Rizzo’s insights at Rizzo Farrugia (Stockbrokers)

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026

Equity participation on the MSE

Meaningful reforms are still needed to revive investor confidence

Malta’s dividend league table

Most retail investors nowadays have an overriding preference to invest in bonds