The secondary market for corporate bonds listed on the Malta Stock Exchange (MSE) remains relatively illiquid as it is characterised by limited daily activity (albeit on the rise over recent years), wide bid-offer spreads across several instruments, and a predominantly buy-and-hold retail investor base. These structural features discourage participation by some high-net-worth investors and also some institutions in view of the difficulty and very slow pace of an orderly exit route.

In view of the steady increase in new issuance on the primary market, it is necessary to have an institution participating in the secondary market to reduce bid-offer spreads across many corporate bonds thereby increasing trading activity. This will inevitably accelerate the development of the Maltese capital market and make this an ideal avenue also for funding some of the major national projects in the years ahead including some that are central to Malta’s Vision 2050 as disclosed in the lengthy document published a few days ago.

In the sovereign bond market, Malta Government Stocks (MGS) benefit from the role played by the Central Bank of Malta (CBM) as a ‘market-maker’ or as some participants define it as a ‘buyer of last resort’. The ‘liquidity backstop’ by the CBM is a critical function in the MGS market. Over the years the involvement of the CBM in the MGS market has demonstrated the effectiveness of a credible public-sector liquidity backstop on the orderly functioning of the market.

In my view, the Malta Development Bank is ideally placed to perform the function of a Liquidity Provider (LP) in qualifying corporate bonds listed on the MSE. Their role as a ‘liquidity backstop’ can be formally defined as the Malta Development Bank Corporate Bond Liquidity Facility (MDB-CBLF). By taking on an analogous role to that of the CBM in the MGS market for qualifying corporate bonds only, the MDB-CBLF can make a meaningful difference to the functioning of the Maltese corporate bond market.

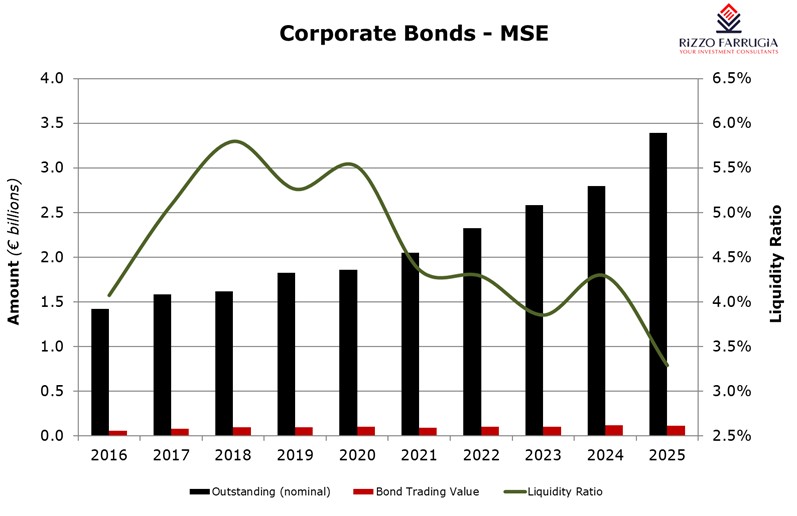

Currently, the total nominal amount of corporate bonds in issue on the MSE is of circa €3.4 billion across 74 bond issuers with 120 listed instruments. However, average daily secondary market turnover in corporate bonds remains negligible relative to the outstanding nominal amount. This is referred to as the liquidity ratio which compares unfavourably to other small European exchanges in countries such as Slovenia, Estonia, Latvia and Lithuania. It has been on a decreasing trend in recent years given the strong rate of growth in new bond issuance which was not also reflected on the secondary market.

Replicating the MGS model in the Corporate Bond Market

Liquidity Providers have an important and strong role to play in the corporate bond market. There is ample evidence of this across most international stock exchanges.

The CBM operates very transparently and publishes indicative bid prices on a daily basis across all MGS’s via its own website. This establishes the yield curve in the Maltese sovereign bond market which then enables market participants to price corporate credit risk against a credible risk-free benchmark rate.

Moreover, by acting as a buyer of last resort in the secondary market, the CBM performs a critical function as it provides a reliable exit mechanism for investors to sell MGS to the CBM which is an important signal for investor confidence.

The involvement of the CBM makes the MGS market (especially at the primary offering stage) extremely popular with all types of institutions (including international) and retail investors especially high-net-worth investors. This is extremely important in the context of the growing debt issuance required by the Government of Malta.

Since credit institutions in Malta or other market participants in the capital markets do not seem to have the appetite for the role of a Liquidity Provider in corporate bonds (possibly also due to the lack of any fiscal incentives that are currently available), the MDB could be the right institution to replicate the role that the CBM plays in the MGS market.

Eligibility Criteria for Qualifying Corporate Bonds

For corporate bonds listed on the MSE to be eligible to form part of the MDB-CBLF, one could propose that they would need to satisfy a specific set of criteria. This could be based on outstanding nominal amount (for example, issue size not less than say €10 million); term to maturity; and most importantly, in my view, that the bond issuer/guarantor has a satisfactory credit assessment according to the MDB's risk scoring model. This would be based on key credit metrics such as interest cover, debt to asset ratio, net debt to EBITDA, etc. Ideally, the established criteria for an issuer/guarantor to be within the qualifying list of corporate bonds of the MDB would be done through a consultation exercise with experts operating within the capital markets industry.

As such, only bond issuers satisfying a pre-established and transparent set of criteria would have its bonds eligible under the MDB-CBLF. This will also help to have a recognised credit assessment or risk scoring in viewing of the ongoing debate on the need for an official credit rating by a recognised credit rating agency. Currently, all corporate bonds listed on the MSE are classified as ‘unrated’ which makes it difficult for inclusion in certain institutional mandates.

Assessing the effectiveness of the MDB-CBLF

The success of the new role of the MDB should be mainly assessed against the secondary market activity in corporate bonds as a percentage of outstanding nominal amounts (the target is to increase this to above the 5 per cent level once again within say two years of implementation).

Moreover, the number and diversity of active secondary market investors (specifically with an increase in the number of institutional investors) and the reduction in the average bid-offer spread for qualifying corporate bonds could be other factors to assess the effectiveness of the LP framework.

Given the strong momentum across the bond market over recent months with many corporate issuers actively seeking alternatives to bank financing and the evident start of mobilisation of savings from bank deposits, this is the right time to actively consider the introduction of the MDB-CBLF and implement such an important function for the corporate bond market. The intermediation role of the capital market is instrumental in Malta’s quest to satisfy the EU’s Savings and Investments Union (SIU) especially in the light of the major national projects being planned.

A better functioning corporate bond market could also attract many more international issuers (which are too small to tap into the larger international exchanges) to use Malta’s capital market which in turn would be a very good business opportunity for the MSE. This will also provide increased international diversification for Maltese retail investors who tend to rely solely on domestic issuance via their custody relationship with the Central Securities Depository of the MSE.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Equity participation on the MSE

Meaningful reforms are still needed to revive investor confidence

Malta’s dividend league table

Most retail investors nowadays have an overriding preference to invest in bonds

Continued operating progress at Farsons

Farsons’ beverage business delivered another year of record revenue and higher profitability in FY2025/26