Over recent months I was highly critical about the state of the local capital market and also described it as moribund. However, the events over the past ten days brought back a level of excitement to the equity market that had not been evident in a very long time.

First, there was the confirmation early last week that the subsidiary of Hili Ventures Ltd, Marsamxett Properties Ltd, will be proceeding with a takeover bid of Tigné Mall plc after building up a stake of just under 50 per cent over the past 11 months. This development may have been expected given the financial strength of the Hili Ventures Group and its wide portfolio of properties in various jurisdictions which are all fully-owned.

However, the revelations of last Wednesday 11th September across the banking sector were very much unexpected and created significant attention on the capital market with numerous posts across various parts of the media – both traditional media as well as social media channels. I do not feel it is correct to opine on the subject matter without having all details of the rumoured acquisition or merger of the two banks to enable me to comment accordingly.

Over the years, there were five previous takeover bids that took place across the local capital market. In some instances, namely in the cases of Crimsonwing plc, 6pm Holdings plc and Island Hotels Group Holdings plc, the final result was a full acquisition by each of the offerors and a subsequent delisting of the target company. In other instances, namely in the cases of FIMBank plc and GO plc, this merely resulted in the offeror acquiring additional shares and the target company remaining listed on the Malta Stock Exchange.

Marsamxett Properties Ltd acquired its initial stake in Tigné Mall plc on 9th October 2023, when it obtained a 12.81 per cent holding in the company at a price of €0.82 per share. Almost one month later, Tigné Mall plc announced that Marsamxett Properties Ltd acquired a further 16.73 per cent of the total shares in issue with the result that the subsidiary of Hili Ventures increased its stake to 31.63 per cent of the company. In line with the Capital Markets Rules, no further announcements of this nature took place which enabled the market to be aware of further acquisitions. However, the 2023 Annual Report of Tigné Mall plc published on 22th April 2024 indicated that as at 31th December 2023, Marsamxett Properties held 33.31 per cent of the company which had then increased to 39.29 per cent as at the date of the publication of the Annual Report in April 2024. By then, therefore, Marsamxett Properties became the single largest shareholder of Tigné Mall plc surpassing MAPFRE MSV Life plc which still currently owns 35.46 per cent of the issued share capital.

In the announcement published last Tuesday informing the market of the intention to launch a bid which was then formalised last Friday via the publication of the Offer Document, Marsamxett Properties Ltd confirmed that it currently holds 49.68 per cent of the total issued share capital of Tigné Mall plc. Since April therefore, Marsamxett Properties acquired a further 14 per cent of the company. Essentially, the free float (the amount of shares in public hands) of Tigné Mall plc has been reduced to just under 15 per cent as a result of the various acquisitions that took place.

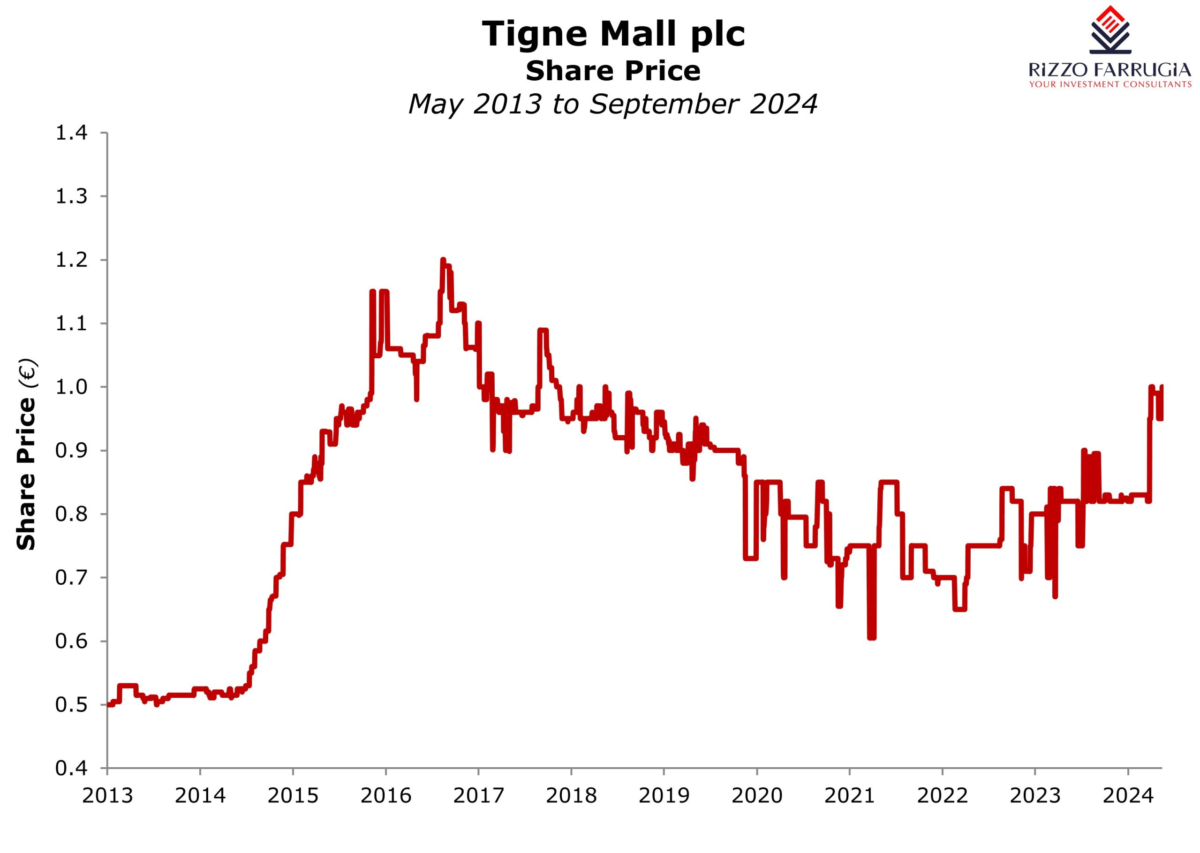

The offer available to all shareholders including MAPFRE MSV Life plc is of €1.04 per share. The share price of Tigné Mall plc has not traded at this level since February 2018. It had reached an all-time high of €1.20 in December 2016 at a time of the very low interest rate environment when many equities offering consistent dividends were being viewed as good alternatives to the low-yielding bonds on offer. At the start of the pandemic in early 2020, the share price of Tigné Mall plc was at around the €0.90 level and reached a low of €0.605 on 19th July 2021.

More importantly, the offer by Marsamxett Properties Ltd of €1.04 per share is equivalent to a premium of 26.8 per cent compared to the €0.82 level which was the price at which Marsamxett Properties acquired most of its stake over the past 11 months.

The latest financial statements of Tigné Mall plc as at 30 June 2024 indicate that the Net Asset Value per share stood at €1.121.

The price to net asset value or book value is a frequently-used metric across the commercial property sector. However, when analysing this offer by Marsamxett Properties in the context of the latest published net asset value, one must also take into consideration the two dividends received by shareholders since the end of June totalling €0.0289 per share representing both the final dividend in respect of the 2023 financial year and the interim dividend for 2024. As such, on an adjusted basis, the offer represents a 5 per cent discount to the net asset value.

Commercial property companies listed on the local and international financial markets generally trade at a discount to the net asset value per share. For local investors, a review of the pricing multiples of some of the other commercial properties listed on the Malta Stock Exchange is possibly the best comparison in the context of the current offer of Tigné Mall plc. Currently all companies trade at a discount to their stated net asset value and within this context it is worth highlighting those of Plaza Centres plc (49 per cent discount), Malta Properties Company plc (40 per cent discount) and Hili Properties plc (28 per cent discount).

In some of my recent articles on the state of the local capital market, I mentioned the liquidity of the market and the sharp reduction in trading activity since the pandemic. This is an increasingly important consideration for the investing public who are becoming more appreciative of the need to quickly exit an investment if circumstances so require. With two shareholders currently having 85 per cent of the issued share capital of Tigné Mall plc, the shares in public hands (free float) is likely to decrease further in the coming weeks once the current takeover bid is concluded next month. As such, the investing public needs to be cognisant of the extremely limited trading activity that is very likely to characterise this particular equity following the conclusion of this takeover.

Given the challenging circumstances faced by investors in Maltese equities over recent years, it would be interesting to gauge the reaction to this latest takeover bid which could offer an exit route from a company owning a single asset in a sector which is becoming increasingly competitive.

In the near future, one cannot exclude other takeovers taking place across the Maltese capital market as a result of different shareholder profiles and requirements across various companies. These are interesting times once again for the local capital market. Hopefully, the planned initiatives by the Government in the upcoming Budget will also invigorate additional activity beyond these latest corporate actions and also encourage other companies to list their equity to also replace the inevitable decline in the number of listings that take place via such takeover bids.

Rizzo, Farrugia & Co. (Stockbrokers) Limited is acting as Manager, Registrar, Collecting & Paying Agent in connection with the Conditional Voluntary Public Takeover Offer.

Read more of Mr Rizzo’s insights at Rizzo Farrugia (Stockbrokers).

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026