The interim reporting season is now in full-swing both locally as well as internationally. At the start of the week, Bank of Valletta plc published its financial statements as at 30th June 2024 and delivered a presentation to financial analysts providing a detailed walkthrough behind the financial results.

BOV’s financial performance is always a key focus of attention for the investor community given its dominant position across the banking sector with a market share of deposits currently at over 49 per cent and an equally-important share of over 43 per cent in loans.

When reporting on their 2023 financial statements some months ago I had stated that “the profits of €251.6 million are well-and-truly reflective of a bumper year largely brought about by the increase in interest rates by the European Central Bank”.

This statement is important when placing into perspective the impressive financial performance in the first half of 2024 showing pre-tax profits of €148.2 million (representing an increase of 40.9 per cent over the same period last year). Yet again, this is reflective of the current interest rate environment which boosted the profitability of many local and international banks after a prolonged period of subdued results as interest rates were held at historically low and at times negative levels for several years.

In fact, the main driver of the surge in profitability at BOV during the past six months is once again the net interest income — the difference between the interest that banks receive from loans, investments and cash at the central bank and the interest that they pay on deposits and other liabilities.

During the first half of 2024, net interest income surged by 21.1 per cent to €193.6 million compared to €159.9 million in the first half of 2023 and €352.0 million during the entire 12-month period in 2023.

An analysis of the different components within the net interest income is the most important area of focus for investors since this remains the core business of the bank. BOV’s strategy of balance sheet optimisation was very clear last year as it aimed to partially reduce the bank’s dependency on future changes to the ECB interest rate to the overall interest income of the bank. In fact, this was also clearly highlighted by BOV during the presentation of the Q1 2024 results some months ago and once again earlier this week.

The sensitivity of BOV’s income statements to interest rate fluctuations has reduced materially as there was a major shift in assets into longer term interest-earning instruments. The bank now reported that a one percentage point movement in the deposit facility by the ECB would result in a movement of only €20.8 million in interest income which is significantly lower than the €52.4 million movement based on the balance sheet composition in 2021.

During the first six months of 2024, further substantial progress was made in this respect as cash and short-term funds decreased by €1.1 billion (now at €1.2 billion from over €5.2 billion in 2021) and these were redeployed in longer-term interest-earning assets. The bank’s proprietary treasury portfolio increased by a further €723.2 million to €6.1 billion with loans and advances to customers increasing by €371 million to €6.6 billion.

The increase in net interest income during the first half of the year principally came about from the treasury portfolio with income from this segment rising by €29.8 million. Meanwhile, interest income from the loan book grew by €12.5 million.

The substantial growth in the treasury portfolio over recent years is one of the key strategic initiatives which will enable the bank to sustain annual pre-tax profits of well-over €200 million in the coming years. By shifting a large component of assets that reprice in the short-term to longer-term assets (investment grade bonds and customer loans), the bank locks in returns over a longer-period of time, thereby achieving greater stability over the interest rate cycle.

During this week’s meeting, BOV’s CFO Kevin Cardona highlighted that the income from the treasury portfolio is currently averaging circa €30 million per quarter with an effective interest rate of 2.1 per cent.In essence, this implies that the treasury portfolio will be generating annual income of €120 million compared to much lower levels in the region of just over €20 million annually between 2020 and 2022. This will provide less sensitivity to interest rate fluctuations by the ECB. This major achievement is probably overlooked by the investor community and will become more evident over the coming reporting periods.

Following the surge in profits, the main key performance metrics remained exceptionally strong. The net interest margin (NIM), which is the difference between the rate charged on loans and that paid on deposits, expressed as a percentage of interest-earning assets stabilised at a healthy 2.7 per cent. The post-tax return on average equity of 15.5 per cent increased from 12 per cent in the first half of 2023. Likewise, the loan-to-deposit ratio improved to 53.4 per cent and the cost to income ratio also strengthened meaningfully to 40.7 per cent

The share price of BOV immediately reacted positively to the publication of the financial statements earlier this week as it surged 6.8 per cent to a six-year high of €1.58. BOV’s market capitalisation has now surpassed €920 million placing the bank firmly as the largest company whose equity is listed on the MSE.

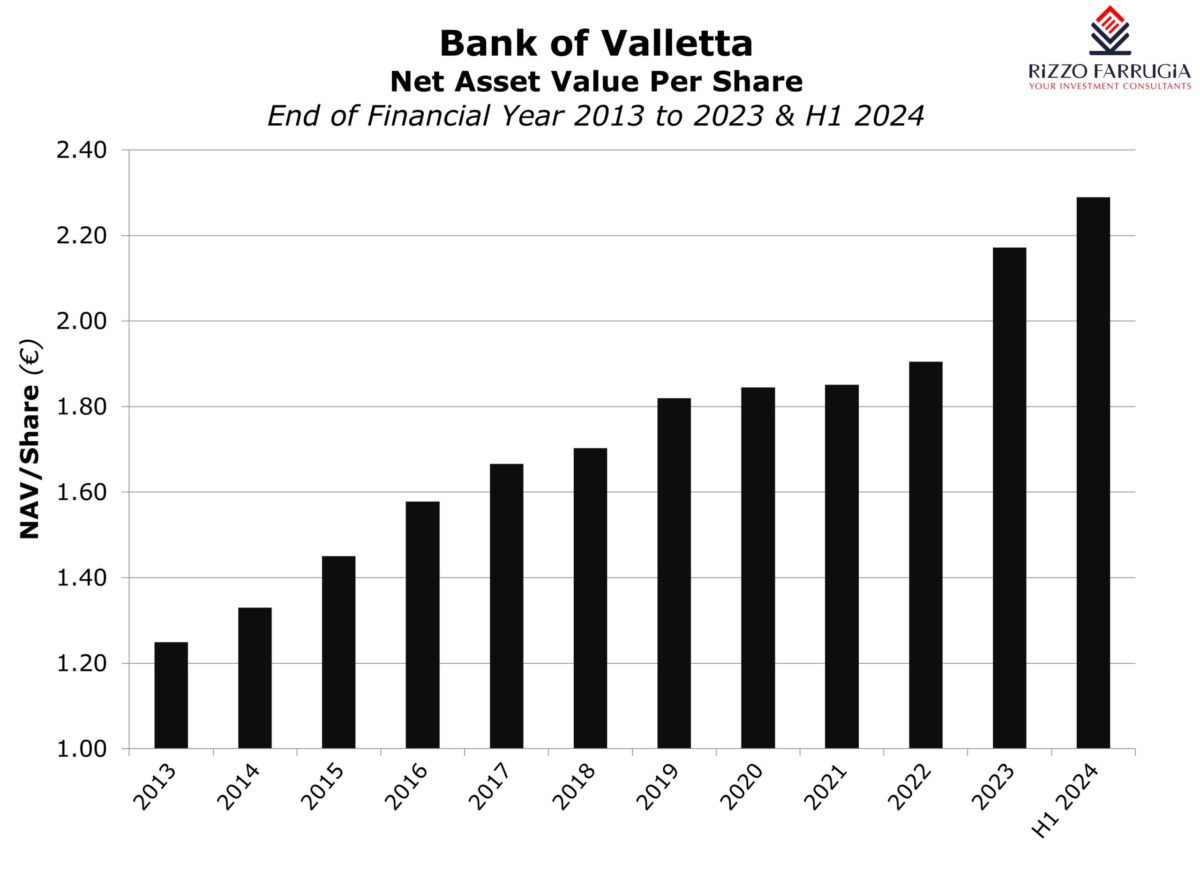

As I commented earlier this year, BOV’s share price has been trading below its book value ever since 2017. Despite the strong share price performance over recent days and months, it is still 31 per cent below its NAV of €2.289 per share as at June 2024. Essentially, the jump in the share price this year (+11 per cent) was largely mirroring the growth in the net asset value as a result of the strong profitability levels.

Earlier this week, BOV did not declare a dividend to shareholders. In the announcement, BOV reiterated that “it will be undertaking a study to assess the feasibility of initiatives intended to optimise shareholder value” which will be concluded by the end of October. The announcement clearly highlighted that the possibility of a share buyback programme will be apart from the “the imperative to sustain a healthy cash dividend”. During the meeting with analysts, BOV’s Chairman Dr Gordon Cordina indicated that a similar procedure to last year will be adopted which would pave the way for BOV to have a semi-annual dividend in place with the interim dividend in Q4 of the financial year and the final dividend in May after shareholders’ approval at the Annual General Meeting.

Possibly, the major surprise from the announcement earlier this week was the upcoming launch of a Medium-Term Note Programme of up to €250 million. BOV’s strong growth trajectory requires a constant need for capital in line with regulatory requirements.

A number of interesting developments will be taking placing concurrently in the final quarter of the year with these new fixed-income instruments being launched coinciding with the completion of the study on optimising shareholder value as well as the confirmation of an interim dividend.

Read more of Mr Rizzo’s insights at Rizzo Farrugia (Stockbrokers).

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026