All asset classes were severely impacted last month following the conflict in Iran which erupted in late February. Within days, the Strait of Hormuz – the narrow maritime chokepoint through which roughly one-fifth of the world’s oil supply transits daily – had been effectively closed to commercial shipping.

Although sovereign bonds are normally perceived as a ‘safe haven’ in times of conflict with an assumed upward movement in prices, the immediate reaction in the bond market since the start of the conflict on 28th February has been precisely the opposite.

Why are sovereign bond prices falling

The war in Iran resulted in an energy supply shock to the global economy. Brent crude, which was trading around USD73 per barrel on the eve of the conflict, surged to above USD110 per barrel – a gain of more than 55 per cent within a month. Natural gas prices also jumped in a similar manner.

The impact on inflationary expectations was immediate as higher energy costs feed directly into consumer prices, threatening to push inflation well-above the 2 per cent targets maintained by most of the major central banks.

The strong reaction in the bond market encapsulates the fear of a return to the stagflationary dynamics last experienced in 2022 – or, in a more adverse scenario, an echo of the energy crisis of the 1970’s. In view of the risk of higher inflation, investors are demanding compensation through higher bond yields.

The surge in yields

Given the inverse reaction between yields and prices, the sharp upturn in yields translates into lower bond prices. This was evident across all sovereign bond markets worldwide.

In the US, the benchmark 10-year Treasury yield rose from approximately 4.0 per cent prior to the conflict to 4.45 per cent – an increase of 45 basis points (bps) within the space of a month. The 2-year Treasury note, closely tied to Federal Reserve policy expectations, climbed from below 3.5 per cent to above 4.0 per cent. Most market commentators are now not expecting any interest rate cuts from the Federal Reserve in 2026 – a significant contrast from the expectations of one or two rate cuts before hostilities commenced.

In Europe, the movements in some sovereign bond markets have also been significant. Germany’s 10-year Bund yield – the risk-free benchmark for the euro area –surged from approximately 2.65 per cent to around 3.1 per cent. This naturally impacted other bond markets across Europe including Malta.

Italy’s 10-year borrowing costs climbed above 4.1 per cent (their highest since mid-2024), representing a rise of almost 80 basis points last month, a move comparable in scale to the region’s last energy crisis of 2022. France’s 10-year yields touched a high of nearly 3.9 per cent (their highest level since 2009), while Spain’s 10-year yield rose to over 3.6 per cent for the first time since late 2023.

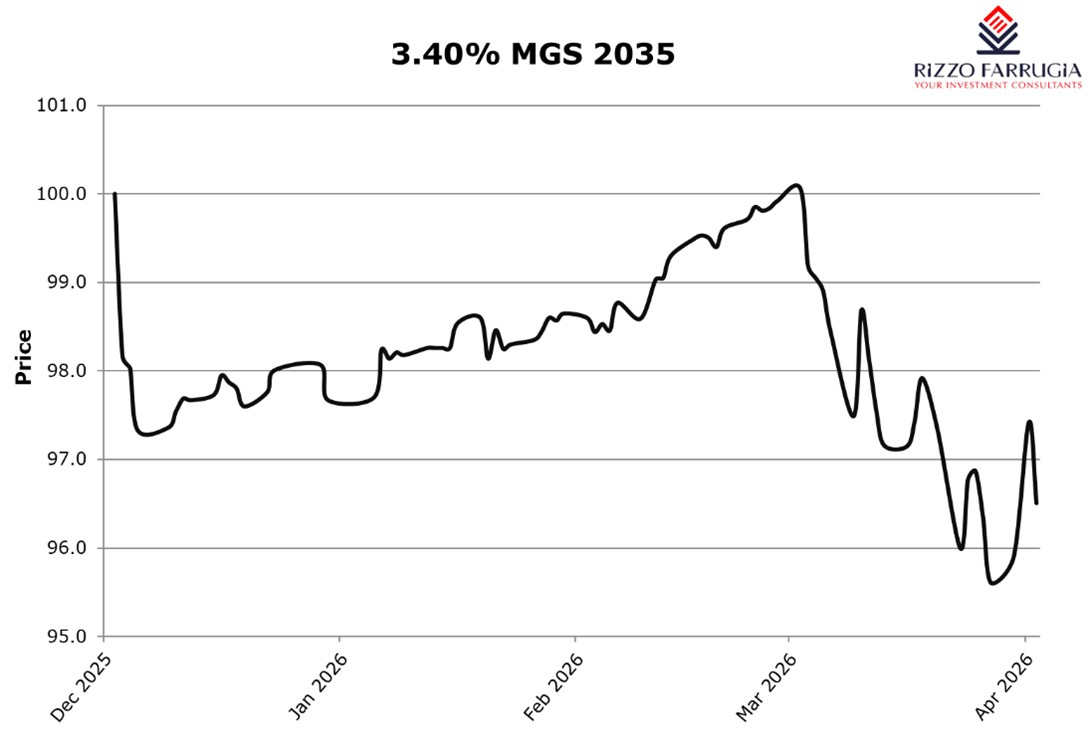

Since the daily indicative Malta Government Stock (MGS) prices quoted by the Central Bank of Malta are based on the movements across the eurozone, the surge in yields was also evident in Malta. The yield of a 10-year MGS jumped from 3.53 per cent on 27 February to over 4.05 per cent towards the end of March.

In terms of price movements, this is reflected in the indicative bid price of the 2.5 per cent MGS 2036 which slumped to 86.58 per cent from 90.87 per cent at the end of February.

The movement in sovereign spreads – the additional interest premium that investors demand to hold the bonds of so-called peripheral eurozone economies over German Bunds – has also been noteworthy. Italy’s spread over Germany was approximately 60 basis points before the conflict erupted. It has since widened back to almost 100 basis points. A number of market commentators do not believe there are significant concerns over eurozone sovereign risk for now. However, this is dependent on the duration of the conflict and if the fiscal measures being introduced by countries to stem the energy crisis onto consumers will become more expensive. Spain has already approved a tax relief package worth €5 billion, reducing VAT on electricity, natural gas, and fuels from 21 per cent to 10 per cent. Italy has cut fuel excise taxes by 20 per cent in an interim measure costing some €417 million until early April until a further review is considered.

The reaction by the ECB

As expected, during the ECB’s Governing Council meeting on 19 March, the deposit facility rate was left unchanged at 2 per cent. However, the language and projections accompanying the decision were much more cautionary than at any point since the post-pandemic tightening cycle.

The ECB's updated staff projections, which exceptionally incorporated data up to 11 March given the extraordinary circumstances, now envisage headline inflation averaging 2.6 per cent in 2026, 2.0 per cent in 2027, and 2.1 per cent in 2028. This represents a meaningful upward revision from the December projections, which had envisaged inflation remaining just below the 2 per cent target in the next few years. In adverse and severe scenarios with oil prices remaining above USD100 per barrel for a sustained period, the ECB warned that euro area inflation could peak as high as 4 per cent this year and potentially above 6 per cent in early 2027 if energy infrastructure damage proves more severe and persistent. Economic growth, meanwhile, has been revised sharply lower to just 0.9 per cent in 2026.

The remarks by the ECB President Christine Lagarde following the meeting on 19 March represented a notable shift from her previous statement that the euro area is in a 'good place.' She stated the Governing Council was "well-positioned and well-equipped to deal with the development of a major shock that is unfolding", while warning that the war "has made the outlook significantly more uncertain" creating "upside risks for inflation and downside risks for economic growth".

In another speech a few days later, the ECB President hardened her tone further, stating that even if the inflation overshoot from the energy shock proved "not too persistent", policymakers stood ready to tighten monetary policy – effectively putting rate hikes back on the table for the first time in over a year.

Market participants are now anticipating that the ECB will raise its benchmark interest rate three times this year. The ECB's next Governing Council meeting is scheduled for 30 April.

Implications for Maltese investors

For many retail and institutional investors in Malta, who have long favoured MGS as a core component of their investment portfolio, the surge in yields in the past few weeks represents a potentially more attractive entry-point into the Malta sovereign bond market in the upcoming new MGS issues being offered to the public later this month.

Following a surprising delay by the Treasury to publish its indicative issuance calendar for this year and the lack of issuance in Q1 in view of the requirement for record issuance in excess of €1.9 billion in 2026, it has now been confirmed that a 10-year and 15-year issuance will take place this month. It is interesting to note that when a 10-year MGS was issued at a yield of 4 per cent in October 2022, there was a record of subscriptions from retail investors amounting to just below €300 million.

This is proving to be yet another very uncertain period for all asset classes. The higher yield that should be available for investors in the coming weeks is possibly one of the few positive highlights from the ongoing conflict in the Middle East.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026