MedservRegis plc published its 2025 Annual Report on 28th April and delivered a presentation to financial analysts on 5th May titled ‘Engineered Growth’. The financial performance in 2025 confirms that the financial turnaround of the past three years is now beginning to translate into more tangible shareholder returns.

This is being supported by a significant reduction in the leverage, the central role of the Malta shore base within the context of the evolving energy and geopolitical map in the Mediterranean as well as the increased geographical footprint of the entire Group.

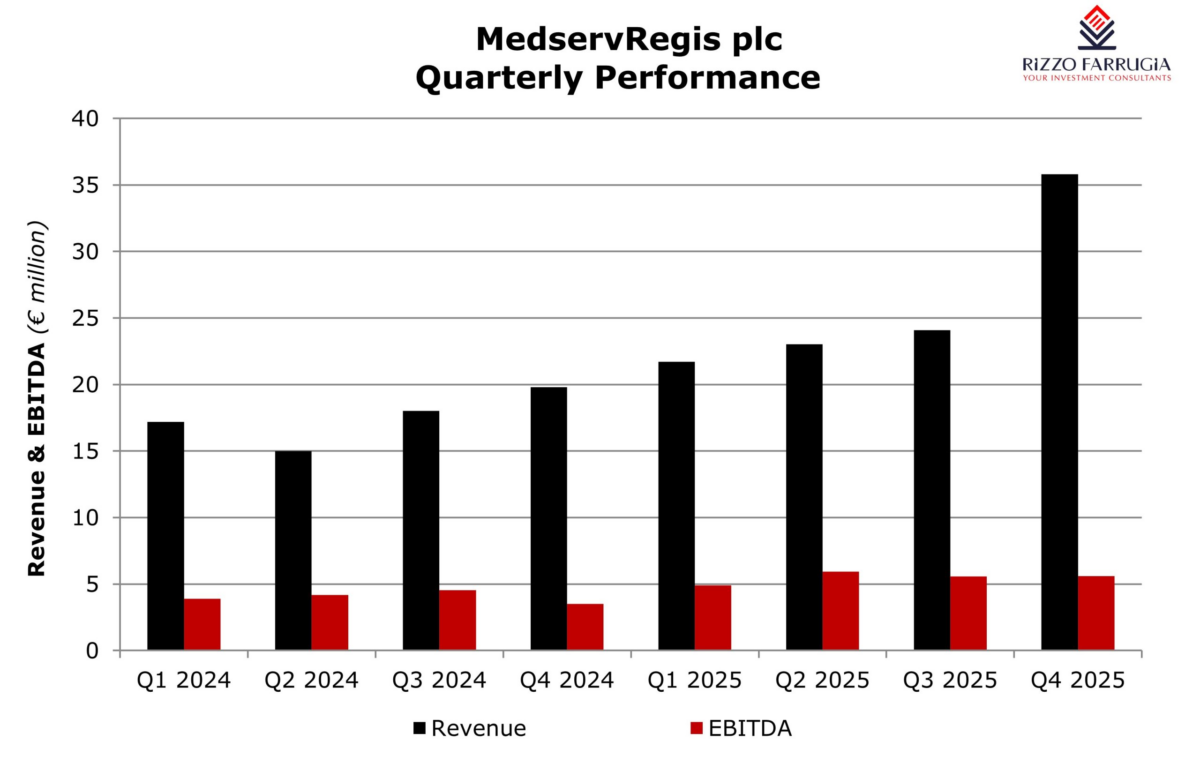

Revenue surged by 49.4 per cent to €104.6 million which materially exceeds the €84.1 million forecast included in the revised Financial Analysis Summary published in October 2025 at the time of the bond exchange programme in Q4 2025. Adjusted EBITDA rose by 36.6 per cent in 2025 to €22.0 million (forecast: €19.5 million) while net profit climbed to €5.5 million compared to a forecast of €4.7 million.

The surge in the ILSS segment

The 49 per cent jump in revenue in 2025 reflects the unprecedented ramp-up at the Malta shore base in conjunction with the works being undertaken for the sizeable offshore Libya drilling programme being conducted by Mellitah Oil & Gas (a joint venture between Eni and the National Oil Corporation of Libya). Moreover, the higher revenue also emanates from the reactivation of the Misurata supply base in the fourth quarter as well as the additional contracts in Cyprus and Egypt.

The Integrated Logistics Support Services (“ILSS”) division accounted for 67.2 per cent of overall revenue at €70.3 million while the Oil Country Tubular Goods (“OCTG”) segment contributed a further 32.4 per cent at €33.9 million.

The ILSS segment was the principal driver of the strong upturn in 2025 with revenue almost doubling from the previous year. This was almost entirely attributable to the Malta shore base (revenue jumped by 219 per cent from the prior year) on the back of the drilling campaigns offshore Libya.

Group operating profit nearly doubled to €12.2 million while the adjusted EBITDA margin edged down to 21 per cent from 23 per cent, reflecting the change in revenue mix as lower-margin logistics work scaled rapidly in the final quarter of the year. Meanwhile, operating cash flow remained strong at €14.8 million and given the capital expenditure of €5.3 million, the Group can easily support both the dividend and the continued focus on debt reduction.

Following the strong outperformance in 2025 compared to the projections published in the October 2025 Financial Analysis Summary, the forecasts for 2026 also published in October 2025 envisaging revenue of €87.0 million and EBITDA of €19.0 million may need to be revised given the ramp-up at the Malta shore base. In fact, the outlook for 2026 provided in the latest annual report confirmed that offshore drilling activity in Libya is expected to remain strong and the Group will continue to build on the momentum recorded across Malta, Egypt, Iraq and Oman. The revised projections for 2026 due to be published by the end of next month should also take into account any revenue from the possible reactivation of the TotalEnergies LNG project in Mozambique, the new long-term premium steel pipe contract in Saudi Arabia, the consolidation of the site support contract in Egypt, and the commencement of the two long-term logistics and agency agreements secured in Suriname covering the period 2026 to 2029.

A transformed balance sheet

The credit metrics of the Group have improved significantly and MedservRegis is now in a fundamentally stronger position to absorb any possible cyclical downturn in the offshore services market. This is a determining factor for shareholders and also bondholders when assessing the creditworthiness and financial strength following the very challenging period over the past several years.

While net debt (including lease liabilities) remained stable at the €50 million level over the past four years, given the surge in EBITDA to €22 million, the leverage ratio improved materially from 4.69 times in 2022 to 2.49 times. Following the repayment of the outstanding bonds amounting to €13.6 million in February 2026, the leverage ratio should improve further in 2026.

The next bond maturity is in December 2029 when the €13 million 5 per cent secured notes are due to be redeemed. This provides ample flexibility for the Board to consider sustained and growing dividend payments while retaining sufficient resources for further capital expenditure and continued debt reduction.

Moreover, during the upcoming Annual General Meeting taking place on 27th May, shareholders are also being requested to consider a share buy-back authorisation of up to 1 million shares (representing 0.98 per cent of issued share capital) within a price range of between €0.65 and €1.10 per share over an 18-month period which is linked to a long-term incentive plan for the newly appointed Co-CEOs covering the three-year period from 2026 to 2028.

The importance of the Mediterranean as part of a wider footprint

The expanding geographical footprint of MedservRegis is another important matter for consideration amid the evolving geopolitical developments impacting the energy sector.

The dramatic resurgence of activity at the Malta shore base supporting offshore drilling campaigns in Libyan territorial waters at unprecedented scale shows the importance of the Mediterranean region. Moreover, the reactivation of the Misurata supply base in Q4 2025 which is a strategically significant development combined with the ongoing contracts in Cyprus and Egypt shows how MedservRegis has effectively positioned itself as the integrated logistics backbone for the Mediterranean offshore industry.

This positioning must be viewed within the context of the growing strategic importance of the Mediterranean as European governments and utility companies are seeking to diversify away from Russian gas.

Beyond the Mediterranean, the OCTG business in the Middle East continues to deliver a solid performance. The expansion into Saudi Arabia under a long-term premium steel pipe contract and the construction of the Abu Dhabi machine shop facility scheduled for completion in 2026, should translate into further profitable growth and consolidate the Group’s position as the principal independent OCTG service provider in the wider Gulf region.

Beyond the core business across the Mediterranean and Middle East, MedservRegis is deliberately positioning itself across some emerging frontier basins. In Sub-Saharan Africa, apart from the presence in Mozambique which could be an important catalyst for 2026 and beyond, MedservRegis has established a presence in Namibia following the important international offshore discoveries by Shell, TotalEnergies and other major oil and gas producers.

In the Americas, the Group has secured two long-term logistics and agency agreements covering Suriname for the 2026 to 2029 period and established a start-up operation in Guyana which is regarded as one of the fastest-growing energy markets.

At the upcoming AGM on 27th May, the shareholders should be attentive on any statements made with respect to (i) the expected duration and scale of the sizeable drilling programme offshore Libya; (ii) given the improved cash flow and with the next bond repayment in December 2029, the capital allocation framework between dividend progression, selective capacity expansion in frontier markets and further debt reduction and (iii) the extent to which the 2026 expected performance will difference from those forecasts published in October 2025 and the actual performance of last year.

The importance for shareholders following the very successful financial turnaround is on how decisively MedservRegis can capitalise on the strong position it now occupies across a number of very important locations within the changing energy market.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026