GO plc published its 2025 annual report on 25th March and presented the main findings to financial analysts last week. GO celebrated its 50th anniversary last year and apart from this important symbolic milestone, the effective completion of the True Fibre rollout across Malta and Gozo was another very important milestone that will be a key determinant going forward.

During 2025, total revenue of the GO Group revenue rose by 3.9 per cent to €254.4 million, EBITDA edged up by 1.5 per cent to €92.0 million and net profit climbed 31.8 per cent to €20.7 million. A final net dividend of €0.09 per share is being recommended for approval at the upcoming Annual General Meeting. Together with the interim net dividend of €0.07 per share paid in September, the total net dividend for the year of €0.16 per share represents a 23 per cent increase from last year’s ordinary distribution of €0.13 per share without taking into consideration the one-off special dividend of €0.15 per share.

When analysing the latest financial statements of the telecoms operator, the cash generation from Malta is a key highlight which can spearhead the Group into a more diversified digital player beyond traditional telecoms.

The investing public needs to start paying close attention to free cash flow generation of GO and other equity issuers on the Malta Stock Exchange to garner a better understanding of the fundamental values of certain companies and the ability for strong dividend distributions.

The Malta cash flow story

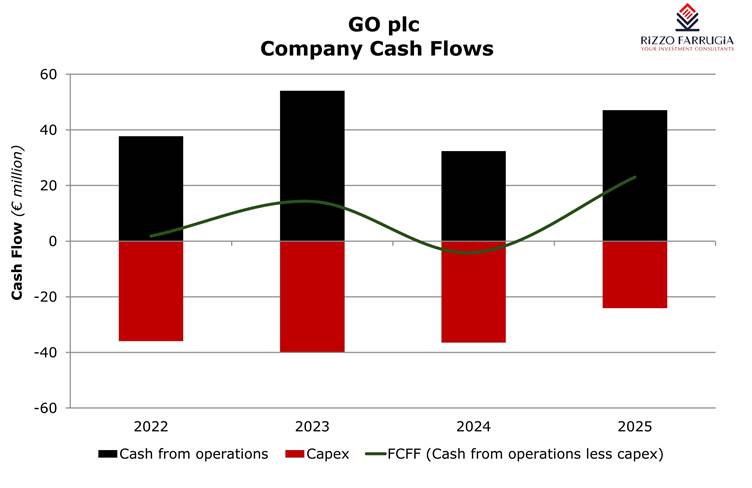

At a standalone level, GO Malta generated €47.1 million in cash from operations in 2025, up from €32.4 million the year before. Capital expenditure fell from €36.5 million to €24.1 million as the True Fibre rollout was essentially completed during the year. Free cash flow amounted to over €23 million which enabled the company to reduce its borrowings by €7 million apart from the payment of dividends and finance costs.

The reduction in capital expenditure in 2025 should not be viewed as a one-off event. Following the True Fibre deployment across the Maltese Islands last year, a more normalised level of capital expenditure is to be expected in 2026 and subsequent years until the next investment cycle will come about especially on the mobile network.

During the upcoming AGM taking place on 19th May, investors should request guidance on the normalised level of capital expenditure in 2026 and also in the following years in order to gauge the extent of free cash flow which is available for the Board of Directors to consider its deployment across a number of areas.

GO’s CEO Mr Nikhil Patil confirmed last week that the investment in the True Fibre rollout enabled the company to upgrade customers and command a higher Average Revenue per User (ARPU) – an important key performance indicator across the telecoms market.

Uses for additional cash

The main focus for the investing public is to obtain insight into the extent of the free cash flow in 2026 and beyond and the possible uses of this growing cash flow.

One of the areas for consideration is undoubtedly Cyprus. At first glance, Cablenet’s performance is disappointing. Revenue fell by 3.3 per cent to €69.7 million, EBITDA declined by 16.4 per cent to €19.1 million and the company generated a loss before tax of €4.2 million denting the overall performance of the GO Group. The mobile subscriber base at the Cypriot subsidiary grew by circa 9 per cent to over 170,000 customers with a market share of 11 per cent while Cablenet’s broadband market share stood at 23 per cent. During last week’s call, the CEO of Cablenet acknowledged that the decline in revenue came about due to piracy issues and amid intense competition in the mobile segment. However, it was also noted that there are positive indications for 2026 with a growth in subscribers already evident translating into “a meaningful overall revenue uplift” following “the strategic investments in network infrastructure and an improved product proposition”.

With the intensifying competition across the 4 players in the Cypriot telecom market and the strategic importance of scale in the mobile segment, one of the obvious areas for deployment of cash by GO is into Cablenet.

During 2025, GO increased its support through additional loans provided to its Cypriot subsidiary. However, given the ongoing developments in the sector, it is obvious that important strategic decisions need to take place in the context of market consolidation initiatives if GO wishes Cablenet to be one of its main engines of growth in the future.

Shareholder returns and leverage is another area to deploy part of the growing cash flow from the Malta business. Over the past seven years, GO distributed in excess of €160 million in dividends to its shareholders. With free cash flow from the Malta business now comfortably covering both immediate capital expenditure requirements and ongoing dividends totalling €16 million based on the FY2025 payout, there is scope for a continued gradual upward progression in the ordinary dividend per share combined with a further reduction in borrowings.

The third area for consideration to deploy part of the excess cash is in the Group’s continued growth beyond telecoms. Non-telecom revenue grew by 12.4 per cent to €68.2 million in 2025 and now represents 27 per cent of overall Group revenue. This is split across data centre services through BMIT Technologies plc (49 per cent), electronics and equipment through Klikk (40 per cent), and other services including cybersecurity, renewables and assisted living (11 per cent). The entry into the insurance segment last year provides a signal of another potential area of focus.

Telecoms customers are a natural distribution channel for other financial products and GO's strong brand equity provides an ideal platform to promote financial products to an existing base of more than 500,000 customers across Malta and Gozo. Continued penetration into specific areas of financial services would be a logical extension of last year’s launch into home insurance and one that fits perfectly with the Group's strategy to capture a larger share of a customer’s digital wallet.

At the upcoming AGM on 19th May, the CEO of GO should clearly guide the market on the normalised level of capital expenditure in 2026 and the following years and the resultant free cash flow being made available from the Malta operations. Nonetheless, in view of its obligations as an issuer of bonds on the Malta Stock Exchange, GO will be publishing a Financial Analysis Summary by 25th May providing forecasts on the Malta operations from which investors can gauge the reduced capital expenditure in 2026 and the estimated growth in the cash conversion.

GO shares can be viewed on the one hand as an investment in a mature, cash-generative telecoms business in Malta that can comfortably sustain a semi-annual dividend to shareholders giving a current yield of over 6 per cent and, on the other hand, a collection of potential growth options in Cyprus, digital infrastructure, and other areas beyond telecoms (energy, consumer retail and financial services) whose eventual contribution to shareholders is still uncertain.

In the meantime, the key drivers and catalysts for the share price and activity in GO shares will be centred around the decisions being taken on the important strategic choices available to the Board of Directors.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Equity participation on the MSE

Meaningful reforms are still needed to revive investor confidence

Malta’s dividend league table

Most retail investors nowadays have an overriding preference to invest in bonds

Continued operating progress at Farsons

Farsons’ beverage business delivered another year of record revenue and higher profitability in FY2025/26