Earlier this month, the Treasury Department announced the issue of two new Malta Government Stocks (MGS) for an aggregate nominal amount of up to €400 million. The two fixed-rate stocks were a 10-year MGS having a coupon rate of 3.40 per cent and a 15-year MGS at a coupon rate of 3.80 per cent. Both were offered to the general public for amounts up to €499,900 per application at par (100 per cent).

Last Friday the Treasury announced that applications from the general public (retail investors) amounted to around €155 million and all applications be accepted in full. The Treasury explained that the final nominal amount that will be allotted to the general public (which will be accepted in full) for each MGS will be published once the vetting of all applications is completed. As such, we are as yet unaware whether the general public had an overriding preference for the 10-year or the 15-year issue.

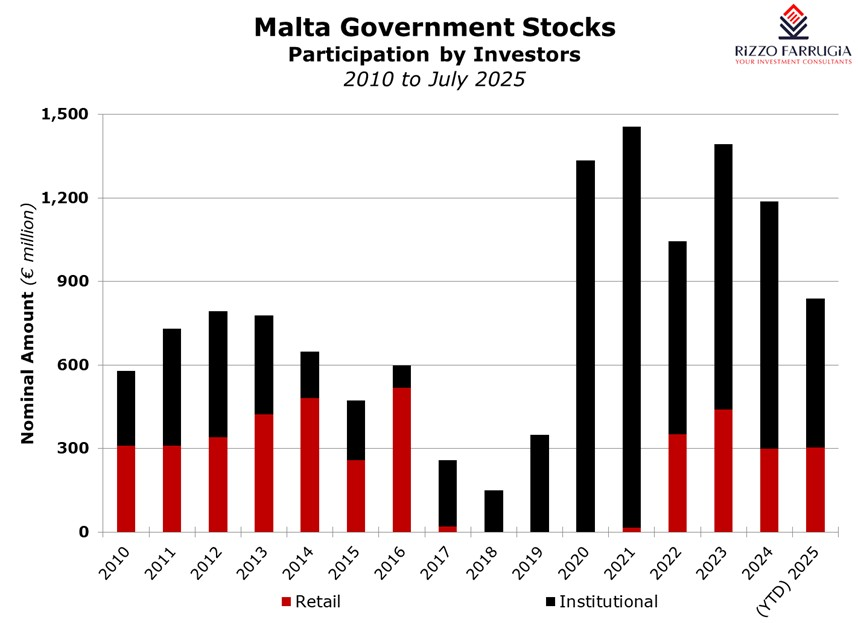

Despite this, the demand from the general public of €155 million was indeed relatively strong. In fact, it was higher than each of the previous five retail offers since September 2023 and only marginally below the €180 million level attracted in the retail offers in both February and July 2023.

While this level of participation may be surprising to some observers, particularly following the record issuance of corporate bonds on the local market in June which attracted €227 million across three bonds, one should also note that resident deposits held with local financial institutions reached an all-time high of €27.2 billion at the end of May and the majority of this money earns zero or very little interest.

Meanwhile, a tendering process took place for applications in excess of €500,000.

The vast majority of bids (€282 million out of €294 million) were submitted for the 10-year MGS, namely the 3.40 per cent MGS 2035 (IV). This was largely expected since most of the auction participants were credit institutions utilising their excess liquidity and thus would not want to lock in funds for 15 years. In fact, none of the local credit institutions bid for the 15-year MGS, where the total bids amounted to a mere €12 million.

The auction results also provide some interesting factors with respect to pricing. The statistics published by the Treasury indicate that €222 million were allotted to institutional investors in the 3.40 per cent MGS 2035 (IV) at prices ranging from a high of 100.25 per cent (translating into a yield-to-maturity of 3.37 per cent) to a cut-off price of 97.30 per cent (YTM: 3.73 per cent).

As in previous MGS auctions, there was a wide range between the highest bid (surprisingly above the fixed offer price of par) and the lowest accepted bids showing diverging views and strategies adopted by the bidders. The price differential between the highest bid and lowest accepted offered represents a difference of 36 basis points (0.36 percentage points) in the resultant yield to maturity which is significant.

Meanwhile, the weighted average price for accepted bids was of 98.3412 per cent, which translates into a YTM of around 3.60 per cent. On average, institutional investors obtained an incremental yield of 20 basis points over the general public. The statistics also indicate that there were other bids amounting to €60 million which were not accepted since the prices were pitched below the cut-off price of 97.30 per cent.

There was a very similar pattern in the auction of the 3.80 per cent MGS 2040 (II). The successful bids ranged from a price of 100.35 per cent (YTM: 3.77 per cent) to a cut-off price of 98.21 per cent (YTM: 3.96 per cent). The weighted average price for accepted bids was of 99.4641 per cent, which translates into a YTM of 3.85 per cent.

This shows that the weighted average prices for both MGS were below the price offered for retail investors. This trend was observed in nearly all auctions that took place since July 2022. This indicates that while institutions are willing to increase their exposure to MGS’s, the prices they are willing to pay are lower than what the Treasury Department is offering to retail investors.

Furthermore, since the Government of Malta needs to raise substantial amounts annually, the Treasury Department is somewhat constrained to accept lower prices (higher yields) to satisfy the funding requirements of the Government of Malta.

In fact, in January 2025, the Treasury Department announced that the amount of MGS issuance during 2025 will be in the region of €1.5 billion, which will be principally used to finance the estimated Government deficit of €850 million and the redemption of two MGS issues and other government loans which in aggregate amount to just under €540 million. To date, the Treasury has issued €450 million in MGS in February and allotted a total of €388.1 million in the July 2025 issue, which indicates that one should expect further issuance of MGS’s exceeding €600 million until the end of 2025.

Furthermore, when considering the forecasted budget deficits of €754 million for 2026 and €700 million for 2027 as indicated in the 2025 Budget Document, coupled with the maturity of over €900 million in Government debt in each of the next four years, it is evident that the annual MGS issuance will continue to remain elevated at well over €1 billion annually and will be a key contributor to new offerings across Malta’s capital market and an important reference for corporate bond issuers.

The size of the budget deficit in the coming years will play a very important role of possible yield movements as investors (especially institutional) may require more attractive yields if Government funding requirements are considered excessive or lead to investor fatigue. Meanwhile, this would be an opportunity for credit institutions to achieve superior yields and possibly higher allocations of sovereign bonds in their treasury portfolio.

Read more of Mr Falzon's insights at Rizzo Farrugia (Stockbrokers).

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026