From the performance of the main indices in the US and Europe, one would think that it was a relatively calm and uneventful start to the year. In fact, the three main indices in the US all registered positive performances with the Dow Jones Industrial Average up by 1.7 per cent while the S&P 500 (after briefly surpassing the important psychological level of 7,000 points) and the NASDAQ ended the month with milder gains of 1.4 per cent and 0.95 per cent respectively. It was also a positive month for all European equity indices with the exception of France’s CAC 40. Spanish and UK equities started the year as best performers with gains of 3.3 per cent and 2.9 per cent respectively in January. The Euro STOXX 50 index advanced by 2.7 per cent in January, reaching a new all-time high of 6,067.50 points mid-month.

However, it was a truly chaotic month on various fronts with severe geopolitical developments especially with respect to Venezuela, Greenland and Iran, President Trump’s erratic policymaking, a currency and bond sell-off in Japan and intense movements in the commodities market.

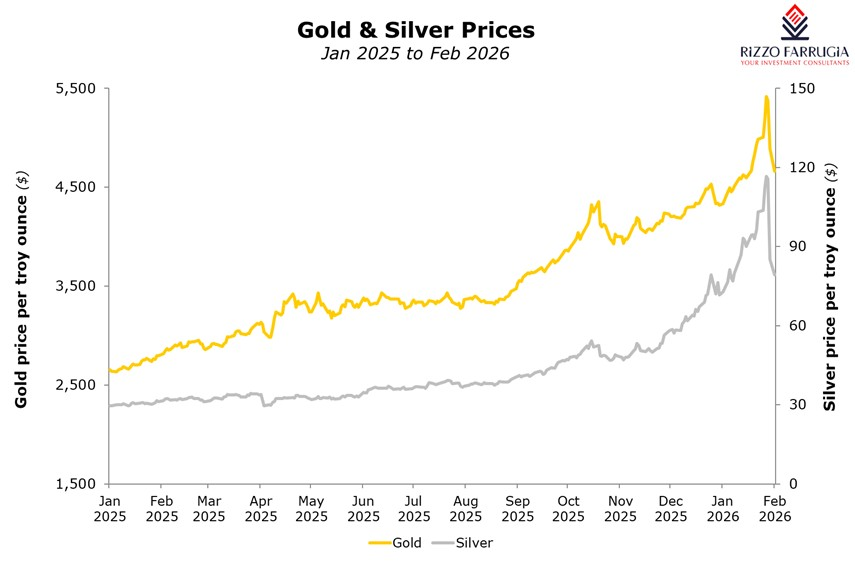

The major factor influencing commodity prices over the past few months has been the elevated macro uncertainty as a result of the various geopolitical developments. Traditionally, a weaker dollar sends commodity prices higher. The US dollar has indeed been on a decline as it dropped by over 13 per cent against the euro in 2025. However, the dramatic scale of the jump in commodity prices and subsequent declines in recent days has been truly historic. The price movements were amplified by the huge increase in popularity of precious metals-backed Exchange Traded Funds (ETF’s) over recent months as the spectacular performance attracted numerous speculators including retail investors.

Last Friday 30th January was one of the most chaotic days for precious metals in decades as there was a historic collapse in prices. The announcement that President Trump nominated Kevin Warsh to be the next Chairman of the Federal Reserve, who is expected to replace Jerome Powell in May, contributed to very sharp declines in gold and silver as the value of the US dollar rose.

Although the potential new head of the US central bank is regarded as an advocate of lower interest rates, he is seen as being less aggressive than some other potential nominees thereby helping the US dollar to regain from the continued downturn seen in recent weeks.

Silver, which had registered a remarkable rally of around 148 per cent in 2025, plunged more than 30 per cent last Friday – its steepest daily decline since March 1980.

Gold also dropped by more than 9 per cent, the steepest one-day drop in spot gold since 1983. Despite the downturn of last week, gold registered its strongest monthly gain since 1999 with an increase of more than 20 per cent.

Gold and silver came under further selling pressure last Monday and extended the sell-off that commenced on Friday.

The sharp movements in gold and silver prompted the intervention of several investment bankers and opinion writers to share their views on the outlook for the year.

Most commentators opined that the main drivers of the gold rally remain intact, including strong central bank demand and lower real interest rates.

Short-term movements in the US dollar will not only be based on ongoing releases of economic data and speculation on how many interest cuts will take place this year but also on official comments from President Trump who last week practically endorsed the recent decline in the dollar.

Among the unprecedented moves across commodities, the earnings season is now well underway in the US, UK and Europe. Many of the largest US technology companies forming the "Magnificent 7" have already reported their results for 2025. The contrasting reaction and share price movements to the announcements by Meta (as it climbed by almost 10 per cent) and Microsoft (its steepest daily decline in 6 years) added further volatility to the events that took place last week. Amazon and Alphabet will be reporting their earnings this week while Nvidia is due to publish its results on 25th February.

The AI theme will undoubtedly remain a key driver for equity performance in the weeks and months ahead. From the earnings reports published to date, it is clear that capital spending on AI continue to grow and there is evident progress toward monetising AI applications.

The events that took place in recent weeks should serve as a lesson to some of the many novice investors regularly ‘following’ international market movements to always be extremely wary of ‘investing’ into popular or fashionable asset classes, sectors or names. Simply because the mainstream media regularly mentions popular asset classes, sectors or individual companies on the grounds of a spectacular performance which creates interesting headlines, should not result in such an instrument being considered as part of a long-term investment portfolio.

There is a wide difference between investing and speculating. Investors must always understand the nature and type of investments they are acquiring and whether these truly fit into their overall objective.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026