The long-anticipated publication of Bank of Valletta’s 2022 annual report took place last Thursday (30th March). Despite accounting for the final sizeable settlement of the Deuilemar litigation of €103 million during the last financial year, the BOV Group registered a pre-tax profit of €48.7 million in 2022. This was permissible as a result of the growth of €45.6 million (29 per cent) in net interest income to €201.9 million and the reversal in expected credit losses of €49.1 million. Some shareholders may be surprised at the overall profits registered in 2022 given the performance until Q3 2022 when BOV had reported a pre-tax loss of €55.7 million for the first nine months of the year.

During a meeting with financial analysts held last Thursday afternoon, BOV’s CFO Izabela Banas explained that the strong improvement in net interest income came about as a result of healthy growth in the loan portfolio which generated additional income of €19.2 million as well as from the change in the interest rate environment which boosted the bank’s core source of revenue by €25 million. Net interest income remains the prime revenue contributor representing 69 per cent of operating income.

The sharp upturn in the deposit facility of the European Central Bank (ECB) during the second half of 2022 is an important tailwind for all banks across the eurozone especially those credit institutions holding sizeable amounts of liquidity. BOV ranks among these banks experiencing a jump in interest income given the high level of liquidity which is amply evident from the loan to deposit ratio of 46 per cent. In fact, an analysis of the net interest income generated on a quarterly basis shows the obvious improvement in the last two quarters of the year (with net interest income of €114.7 million) when compared to the first six months (with net interest income of €87.2 million).

The other major contributor to the overall positive performance in 2022 was the net release of expected credit losses (impairments) which amounted to €49.1 million compared to a net release of €18.9 million in the previous year. The improvement from one year to the next is mainly as a result of a release of provisions (€24.9 million) taken during the COVID-19 period provisions. In the words of CEO Kenneth Farrugia, this reflected, “better economic conditions relative to FY2021 coupled with significant recoveries of past debts”.

For comparative purposes, BOV registered a strong improvement of €71 million (88 per cent) from the pre-tax profit of €80.7 million when adjusting for the final settlement with respect to the litigation in Italy of €103 million. While the profitability of the bank in the previous two years was negatively impacted by the COVID-19 pandemic, the adjusted profit of €151.7 million in 2022 must also be seen in the context of the performance in prior years with record profits in 2016 and 2017.

In view of the concerning developments across the US and Swiss banking sectors during the month of March, it is worth highlighting once again the sheer amount of liquidity held by BOV which reported a liquidity ratio of 426 per cent as at 31 December 2022. The high levels of liquidity across the Maltese banking system was also highlighted by the international credit rating agency Fitch Ratings in its recent update on Malta’s credit rating. Fitch clearly opined that they do not foresee any “immediate risks to the Maltese banking sector from the recent international banking turmoil”. The rating agency was clear in its review that “liquidity levels in the banking sector are exceptionally strong, with Malta reporting the largest liquidity coverage ratio among EU countries as of 3Q22”.

This should continue to reassure the Maltese investing public who should not be swayed by the information overload across social media on the debacle of Silicon Valley Bank and other regional banks in the US given the totally different business models of Malta’s traditional retail banks.

The annual reporting season in Malta which commenced towards the end of February depicted a clear improvement in the financial performance of several companies arising from the strong recovery post-COVID. This led to a number of companies maintaining their dividend distributions such as GO plc, BMIT Technologies plc and HSBC Bank Malta plc while Malta International Airport plc reinstated dividends after an absence of three years.

BOV’s shareholders were also understandably anxious to learn about the decision on any dividend distribution after the difficulties encountered in recent years. During last week’s meeting, BOV’s chairman Gordon Cordina clearly explained that the sizeable settlement of €103 million for the litigation in Italy had an obvious huge bearing on the overall decision. Mr Cordina also argued on the continuous need for the bank to build its capital position even further to enable it to pursue its growth strategy. In his statement in the annual report, the chairman states that the decision not to distribute a dividend is necessary “to support the capital and liquidity of the bank, and to meet the regulatory expectations”. It is therefore clear from this that the decision was also influenced by regulatory considerations. On the other hand however, Mr Cordina also stated that, “once conditions improve, and subject to the guidance provided by the competent authorities, the board intends to re-establish the pattern of stable and predictable distribution of dividends”.

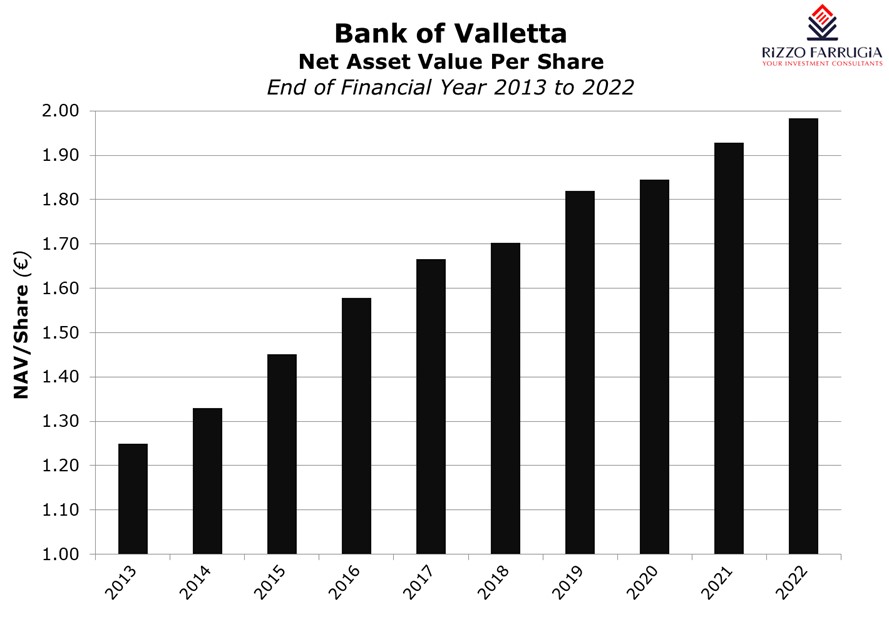

Despite the obvious disappointment that will be felt by a large proportion of the shareholder base on the lack of dividends, they should be comforted at the growth in the net asset value to just over €1.98 per share.

While future announcements of a reinstatement to dividends will be the area of focus to many investors, the performance of the group as a result of the current interest rate environment and how this translates into improved shareholder returns and growth in the net asset value should be the key factors that investors ought to consider when deliberating an investment case in Malta’s largest bank.

Read more of Mr Rizzo’s insights at Rizzo Farrugia (Stockbrokers)

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026