At the end of May 2026, Simonds Farsons Cisk plc published its Annual Report and Financial Statements for the year ended 31st January 2026 and held its annual meeting with financial analysts earlier this week. During the 2025/26 financial year, the spin-off of the food businesses was finalised via the distribution of shares in Quinco Holdings plc to shareholders of Farsons as a ‘dividend in kind’. This is identical to the corporate action of the property business some years ago with a similar distribution of shares in Trident Estates plc.

As a result of the latest spin-off, the food operations are now reported as a discontinued activity within the 2025/26 Annual Report and the continuing operations relate solely to the beverage businesses.

The spin-off of the food businesses led to a €21.9 million fair-value gain which is a large non-recurring item heavily boosting the bottom-line of the 2025/26 financial performance and resultant performance metrics and investor ratios. The total net profit for the year of €39.1 million also includes a net profit from discontinued operations of €2.2 million for the eight-month period of the food business. As such, an analytical review of the 2025/26 performance of Farsons must exclude these one-off line items.

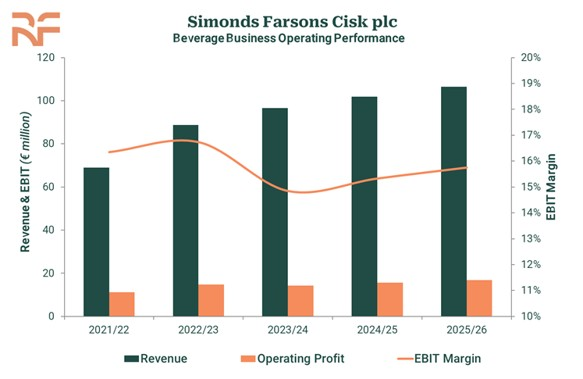

Beverage business revenue rises to €106.5 million

During the 12-month period to 31st January 2026, turnover from the beverage businesses rose by 4.6 per cent to a new record of €106.5 million, thereby continuing the upward trajectory in recent years “despite an increasingly dynamic and competitive operating environment” as described by the directors in the annual report. Over the past two financial years, revenue across the beverage businesses increased by just over €10 million.

The gross margin edged up to 42.7 per cent from 42.5 per cent notwithstanding a 9 per cent rise in selling, distribution and administrative costs as Malta’s exceptionally tight labour market continued to push wage costs higher. The directors attribute the increase in the gross margin to “ongoing investments in efficiency-enhancing initiatives, alongside disciplined and ongoing management of the cost base”.

Operating profit advanced by 7.5 per cent to €16.8 million with the operating margin improving to 15.8 per cent from 15.3 per cent. At the EBITDA level, the beverage businesses generated €24.3 million, which is 5.8 per cent ahead of the prior year.

Profit before tax from the beverage segment improved by 8.2 per cent to €15.9 million. The tax expense for the year amounted to just over €900,000 giving a profit after tax of €15 million.

In his address to financial analysts earlier this week, outgoing CEO Norman Aquilina noted that the positive performance is not reflective of easier market conditions. On the contrary, he mentioned the dynamics of the changing market and ongoing margin pressure but highlighted that the company continued to respond well to the challenges being presented.

There was a significant increase in cash generation during the 2025/26 financial year. Net cash from operations (including the 8-month period of the food business) increased to €22.2 million from €18.8 million in the previous financial year. Net capital expenditure was marginally higher at €11.8 million resulting in a free cash flow of €10.4 million. The capital expenditure of the beverage business alone amounted to just under €7 million.

A continued, gradual increase in dividends

At next week’s Annual General Meeting, shareholders are being requested to approve the distribution of a final net dividend of €0.145 per share (FY2024/25: €0.14) out of tax-exempt profits.

Together with the net interim dividend of €0.065 per share paid in October 2025, the total net cash dividend attributable to the 2025/26 financial year amounts to €0.21 per share, which is 5 per cent higher than the €0.20 per share attributable to the prior year.

The total cash payout to shareholders (of both the interim and final dividends) of €7.56 million translates into a payout ratio of 50 per cent when considering the net profit from continuing operations of €15 million.

Despite the gradual increase in dividends over the years supported by rising profits as well as a higher dividend payout ratio to 50 per cent , the indebtedness of the group has reduced. This suggests clear headroom to continue to lift the payout ratio beyond the 50 per cent level without compromising either the ongoing capital expenditure requirements or the conservatism that has long defined the Farsons balance sheet.

Comparison to forecasts

As a bond issuer, Farsons is obliged to publish its financial projections annually and it is always worth comparing the actual figures against the projections published in the Financial Analysis Summary. The 2025/26 projections were published on 23rd July 2025.

Revenue from continuing operations (beverage) of €106.5 million came in marginally below the €108.0 million forecast – a shortfall of less than 1.5 per cent . Operating profit of €16.8 million was also practically in line with the €16.9 million forecast. Likewise, profit before tax from the beverage businesses at €15.9 million was also very close to the projected €16.0 million.

The strength of the balance sheet

As at 31st January 2026, net debt amounted to just over €19.2 million (largely made up of the €20 million 3.5 per cent bond maturing in September 2027) including lease liabilities of €2.1 million. With the EBITDA of the beverage businesses at just over €24 million in the last financial year, the net debt to EBITDA multiple is of only 0.8 times.

This ratio again confirms that Farsons is effectively under-leveraged. It is generating strong cash flow which could support ongoing capex requirements as well as a more generous distribution policy going forward.

CEO designate Michael Farrugia, who will become CEO as from 1st July 2026, also addressed financial analysts and noted that he is assuming the role with a great sense of responsibility but with confidence on what lies ahead. Mr Farrugia highlighted that it is important for the group to have a culture of continuous improvement and to have robust digital systems in place. Given the dominance of Farsons across the local beverage market, the incoming CEO mentioned the continued quest to grow internationally by pursuing profitable growth initiatives.

The leadership transition with Michael Farrugia stepping up as CEO and Norman Aquilina moving on to Chairman of Quinco Holdings plc comes at an important time. As CFO Anne Marie Tabone noted in her intervention earlier this week, the past financial year was marked by “a strategic refocusing of the group’s principal activities by returning the business to its original routes as a brewer, bottler and importer of beverages”.

The robust performance of the local economy and the very strong increase in tourism bodes well for yet another record year for Farsons. This should be confirmed upon the publication of the Financial Analysis Summary due by the end of July. Particular attention should continue to be given to the margins being achieved to determine the continued success of the group within the evolving market dynamics of the beverage and retail sectors and the ability to maintain a double-digit return on equity. In the next reporting periods, it would also be interesting to note any references to the refinancing plans of the €20 million bond due in September 2027 as well as progress on the master planning of the large parcel of land adjacent to Trident Park.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026