During the course of 2025, I regularly wrote about Malta’s corporate bond market in view of the record amount of issuance last year at over €700 million and also in view of the increased media coverage of the bond market as a result of the well-documented challenges faced by a number of issuers most of which have bonds up for maturity in 2026.

With very strong indications that new issuance activity will also remain robust during the course of 2026, the first article in the new year is also dedicated to the bond market and specifically to the calculation and comments with respect to financial ratios and credit metrics that are of utmost importance for financial analysts and investors to review prior to undertaking any investment decision.

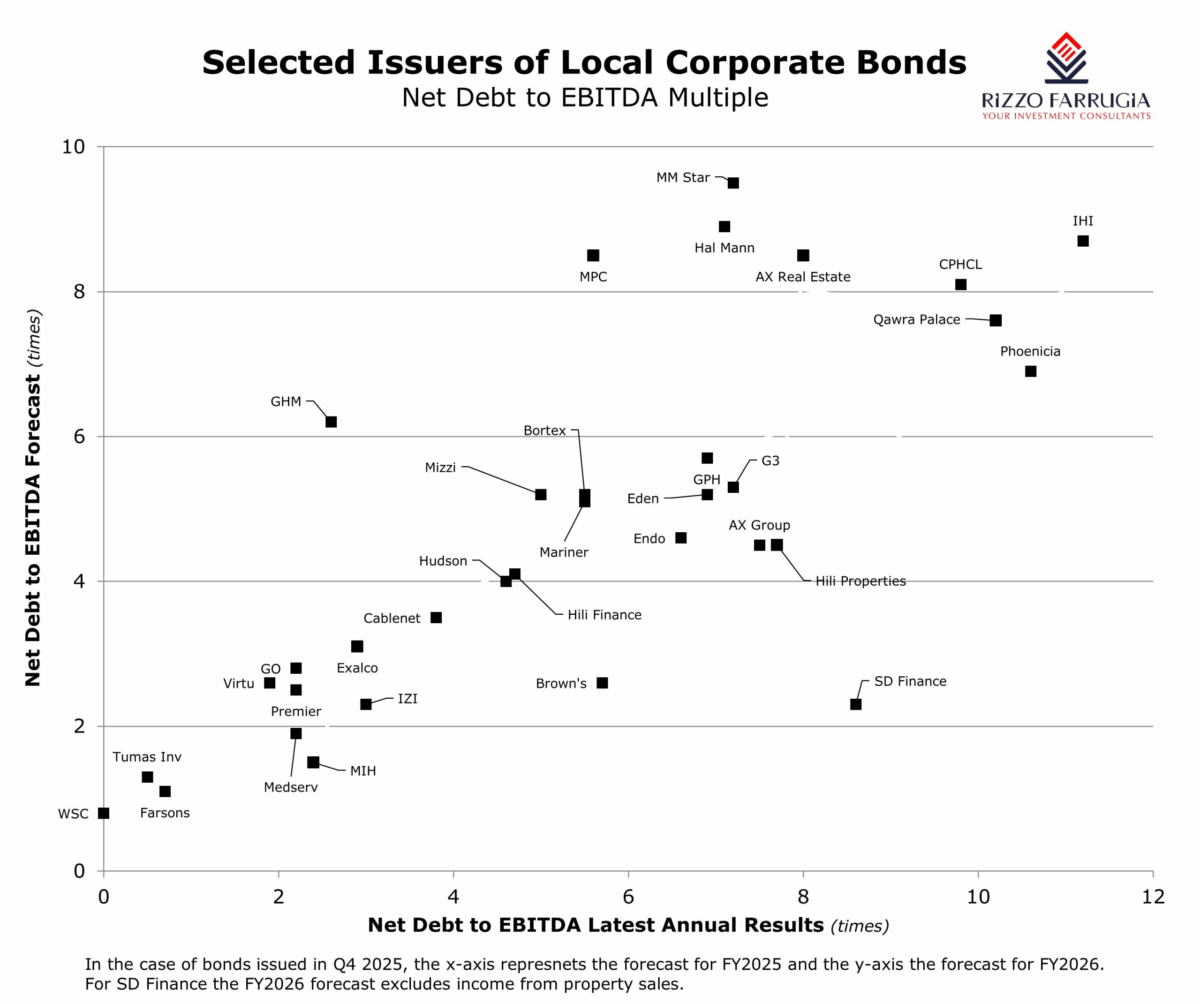

Towards the end of September 2025, I had published an article titled “Assessing a company’s leverage” containing a graph of the net debt to EBITDA multiple of a selected list of issuers or guarantors of local bonds.

This ratio measures a company’s debt burden relative to its earnings before interest, taxes, depreciation, and amortisation (EBITDA) by calculating the number of years it would take for a company to pay-off its entire debt burden assuming the present level of earnings remains unchanged. A low ratio indicates that a company can easily pay-off its debt in a few years while a high ratio provides a clear warning to investors that a company has a high debt burden.

I had also made reference to the parameters adopted by international companies for their leverage ratios and commented that a large number of companies whose bonds are listed on the Malta Stock Exchange (MSE) have a net debt to EBITDA multiple of below 5 times which is therefore very reassuring for the investing public.

Since the article in September, there were some companies that recently published their Financial Analysis Summary (FAS) providing updated forecasts for 2026 mainly in view of new bond issues during the last quarter of 2025. The new bond issues that took place were by SD Finance plc, MedservRegis plc, Central Business Centres plc while Hili Finance plc published a prospectus in December for an issue taking place now. Meanwhile, IZI Finance plc also published its updated Financial Analysis Summary since its financial year-end is 30th June.

The updated figures by these companies depict important observations that the investing community should take note of. Most of these companies noted robust figures with the net debt to EBITDA ratio of MedservRegis plc anticipated to decline to just below 2 times in 2026, the guarantor of SD Finance plc expecting an adjusted net debt to EBITDA of 2.3 times when excluding the contribution of the property sales within the ORA Residences project and Hili Ventures showing consistently strong financial performances with a net debt to EBITDA projected at 4 times in 2026.

However, it was disappointing to note that in the FAS of Central Business Centres plc, the net debt to EBITDA of 19.4 times was defined as “healthy”.

Although there is always an element of subjectivity in the interpretation of credit metrics and financial ratios, a net debt to EBITDA of above 19 times is truly exorbitant and cannot be subject to much interpretation. This implies that it will take over 19 years of the current level of profits for the company to repay its borrowings.

This high debt burden exposes the company to an elevated risk of refinancing when their current bonds or bank loans are due to mature. Essentially, CBC is expected to have ended 2025 with a net debt figure of over €44 million and to have generated EBITDA of €3.4 million from its various properties. The FAS also provides forecasts until 2027. While the net debt figure is expected to peak at over €45.7 million in 2026 following the anticipated issuance of a further €16.5 million in bonds, given the expectation that the company’s financial performance will improve with the EVBITDA anticipate to rise to €5.1 million mainly as a result of improved revenue from Valletta (Savoy), the net debt to EBITDA is forecasted to improve to 8.5 times in 2027.

Although I will always continue to advocate that companies with recurring revenue streams ought to have long-term borrowings in place to optimise their capital structure, a net debt to EBITDA figure of 19 times is truly elevated by any standards or benchmarks used whether these are performed by the international credit rating agencies as part of their financial risk assessment or other scoring mechanisms devised locally.

The introduction of the FAS many years ago was a truly great initiative by the Malta Financial Services Authority (MFSA) for the investing community to have access to forecasts and also to have calculations of ratios to enable investors to assess the progress and financial strength of a company and ultimately make better-informed decisions.

It is therefore surprising that a net debt to EBITDA of 19.4 times was allowed to be defined as healthy once this document was reviewed by the MFSA prior to its recent publication.

In many of my articles and in several seminars that took place during the course of 2025, the need for investor education was correctly highlighted as a top priority for the capital market. In my view, there also needs to be a conscious drive that the right terminology is used by financial intermediaries and all market participants in the important documents that are intended to act as educational tools for the investing public.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Will the ‘magnificent seven’ become the ‘peace makers’ between the USA and Iran?

Financial markets have always had a seat at the table in wartime

Maltese MEPs hail EU anti-corruption law as milestone for business transparency

EU countries will now be required to align their national legal frameworks

Investing in times of war

What does Warren Buffett teach us about investing during conflicts?