The initial Malta Government Stock (MGS) issuance for 2026 took place last week with the Treasury successfully raising approximately €499 million across new 10-year and 15-year bonds as it exercised the over-allotment option of €200 million in full.

The statistics published by the Treasury provide a number of important observations with direct implications for the wider MGS market structure amid the record issuance required this year.

European credit institutions were allotted €228 million of the €290 million within the competitive auction allotment representing 78.6 per cent of the auction and implying an accelerating trend of foreign bank participation to that observed during the course of 2025.

Strong retail demand

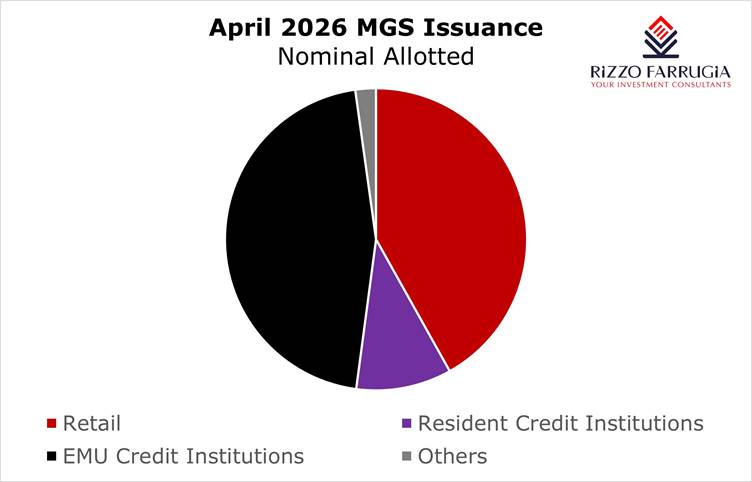

Retail applicants – those submitting non-competitive applications up to a maximum of €499,900 at the fixed prices of 100 per cent (par) across both the 10-year and 15-year bonds – subscribed for a combined nominal of approximately €209 million. This is a strong retail turnout which continues to demonstrate the well-established appetite of Maltese savers for sovereign exposure amid growing idle deposits across the banking system and a clear signal of the added demand for MGS’s as yields edged higher over recent weeks.

The strong take-up by retail investors must be again viewed in the context of the short offer period of less than a week which could limit retail mobilisation and the ongoing competition from new corporate bond issuance which has subsided in recent weeks despite the strong start to the year.

The competitive auction

The results of the competitive auction provide important findings from both a pricing perspective as well as in the context of investor appetite. The aggregate bid-to-cover ratio of the auction was of 2.35 times as demand amounted to €684 million compared to the €291 million on offer after satisfying all retail applicants.

The 10-year 3.80 per cent MGS 2036 (III) attracted exceptionally strong institutional demand. The Treasury received 40 bids totalling €556.5 million – against which only €171 million were allotted across 9 accepted bids. The cut-off price was established at 99.25 per cent (YTM: 3.89 per cent) implying that bids of over €385 million were priced below this level and therefore rejected.

The highest accepted bid was at the same retail offering price of 100 per cent (par), and the weighted-average price across the accepted bids was 99.38 per cent (YTM: 3.88 per cent). The spread between the institutional weighted-average yield of 3.88 per cent and the retail yield of 3.80 per cent was therefore of only 8 basis points – a reasonable level of concession to institutional investors and broadly consistent with historical auction patterns.

The results of the 15-year 4.10 per cent MGS 2041 (II) present a notably different picture. The Treasury received only 19 bids totalling €127.5 million, of which 15 were accepted at an aggregate allotment of €119 million. Essentially, almost all bids received on the 15-year paper were accepted with the cut-off price at 97.39 per cent (YTM: 4.33 per cent) and a weighted-average accepted price of 97.59 per cent (YTM: 4.31 per cent). The spread of 21 basis points between the institutional weighted-average yield of 4.31 per cent and the retail yield of 4.10 per cent was wide as institutional investors demanded much higher yields which is consistent with the global re-pricing of duration risk observed across euro area sovereign bonds over the past months.

Foreign banks dominate the auction

European credit institutions were the dominant buyers of the new MGS offerings last week as they were allotted €228 million of the €290 million total auction allotment across the two MGS’s. This represents 78.6 per cent of the entire competitive auction allotment – by far the highest concentration of foreign bank participation observed in any single MGS issue in recent years.

The breakdown by maturity also provides valuable insight given the record issuance required for this year. In the 10-year issue, the 3.80 per cent MGS 2036 (III), European credit institutions submitted 6 bids for a total of €302 million, of which 2 bids amounting to €122 million were accepted. This represented 71.3 per cent of the €171 million total auction allotment in that maturity. Resident credit institutions submitted 19 bids for a total of €230 million, of which only 5 bids amounting to €45 million were accepted – 26.3 per cent of the allotment in that maturity.

In the 15-year issue, the 4.10 per cent MGS 2041 (II), the concentration of foreign bank demand is even more pronounced. European credit institutions submitted 4 bids for a total of €113.5 million, of which 2 bids amounting to €106 million were accepted – an extraordinary 89.1 per cent of the €119 million total auction allotment in that maturity. Resident credit institutions took just €6 million (5 per cent of the allotment).

Two other findings from the statistics published deserve particular emphasis. Firstly, the absolute number of accepted bids from foreign credit institutions is extremely small – just 2 accepted bids in each bond. This means that potentially as few as two European banks took up €228 million of the MGS’s on offer and it is not implausible that the same two institutions participated across both maturities. This level of concentration represents a meaningful single-source dependency and should be monitored closely as a structural feature of the MGS market going forward.

Secondly, the 19 bids submitted by Maltese credit institutions on the 10-year paper (totalling €230 million) of which only 5 were accepted (€45 million), indicates that local banks were bidding below the cut-off price of 99.25 per cent. This implies that they were bidding at yields meaningfully above those at which foreign banks were willing to participate. This provides further evidence that local credit institutions are displaying greater price discipline than their European counterparts at current yield levels.

Implications for additional 2026 issuance

The increased participation by European credit institutions is a clear signal of support given Malta’s credit rating, its continued strong economic performance and relatively low debt to GDP ratio compared to the EU average. This should not be a major surprise given the structural shift in the MGS investor base evident last year as I had highlighted in an article following the previous MGS offering in November 2025

However, the extent of the increase and their dominance in last week’s offerings provides important implications to policymakers.

In 2025, European credit institutions subscribed for €295 million across the three MGS issues of 2025 representing 23 per cent of total MGS issued during the year. Their participation accelerated materially throughout the course of the year (€51.5 million in February 2025, €77 million in July 2025 and €166 million in November 2025). The November 2025 auction in particular saw foreign banks concentrated at the longer end of the curve, with €82 million of the €86.5 million allotted in the 15-year bond (the 3.80 per cent MGS 2040), compared to zero participation by local credit institutions in that maturity.

Against this backdrop, the €228 million allotted to European credit institutions in the April 2026 auction is a marked intensification of recent trends representing approximately 46 per cent of the total nominal allotment of the April 2026 issue of €499 million. This is an important new structural characteristic of the MGS market with implications for the wider investing community and also policymakers given that the ability of the Treasury to successfully issue long-dated MGS paper (beyond 10 years) is becoming contingent on international institutional demand.

The next MGS issuance is likely to take place during the month of June given the redemptions of just over €535 million between early July and early August. Apart from the movements in yields in the coming weeks, it would be interesting once again to analyse the take-up given the important trends evident over recent months.

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Persistent volatility in euro area bond yields

The instability across the energy sector which impacts inflation expectations is leading to consistent volatility in sovereign bond yields.

The importance of free cash flow

Edward Rizzo urges equity issuers to provide guidance on free cash flow in their communications to the market

Chip stocks lead the bull market

International equity markets performed very strongly during the first half of 2026